Learn more about everything Lightstone DIRECT has to offer

Generating magic link...

The Bonus Depreciation Whiplash: From 40% to 100% and What the OBBBA Means for Real Estate Investors

The following does not constitute tax advice. Please consult with a licensed tax professional when considering the tax implications of private real estate investments.

In December 2024, a real estate tax advisor I know spent half her billable hours telling clients to close, close, close before year-end. The reason was simple, if a little exhausting. Bonus depreciation was on a schedule. After hitting 100% in 2022, it had been stepping down — 80% in 2023, 60% in 2024, and on track to drop to 40% in 2025, then 20%, then nothing. Real estate sponsors with cost segregation studies queued up were scrambling to get assets placed in service before the calendar turned. Limited partners were calling their CPAs at night to ask if a December close was still feasible. It had the energy of a Black Friday sale, but for tax shields.

Then, in July 2025, Congress passed the One Big Beautiful Bill Act, and 100% bonus depreciation came back — retroactively, for property both acquired and placed in service after January 19, 2025, and on a permanent basis for new property going forward. The clients who had rushed to close at 40% suddenly found themselves at 100%. A few even called their CPAs to ask, slightly sheepish, if they could redo the math. The CPAs, who had not made the law, said yes.

This is, on its face, good news for accredited investors in private real estate. One hundred percent bonus depreciation, paired with a cost segregation study, is the single most powerful piece of timing-arbitrage available in the U.S. tax code today. It doesn't make a bad deal good. It does change the year-one math on a good deal in ways worth understanding — and it does so in a way that public-market real estate vehicles cannot replicate.

What the OBBBA actually changed

Bonus depreciation is a Section 168(k) provision that lets taxpayers deduct a large percentage of the cost of qualifying property in the year it is placed in service, rather than spreading the deduction over the asset's useful life. The Tax Cuts and Jobs Act of 2017 set the rate at 100% through 2022, with a planned phase-down:

- 2022: 100%

- 2023: 80%

- 2024: 60%

- 2025: 40%

- 2026: 20%

- 2027: 0%

Tax planners had been working against that schedule for three years. The One Big Beautiful Bill Act, signed July 2025, did three things at once. It restored 100% bonus depreciation for qualifying property both acquired and placed in service after January 19, 2025. It made that 100% rate permanent rather than re-instating the old phase-down. And it added a new category — "qualified production property" — that extends 100% expensing to certain manufacturing and production-use buildings that would otherwise depreciate on a 39-year schedule.

One wrinkle worth flagging. Property placed in service between January 1 and January 19, 2025 stays at the pre-OBBBA 40% rate. It is a narrow window, but it is a real one for any deal that closed in the first three weeks of 2025. The IRS issued interim guidance on the timing rules in Notice 2026-11.

Why this matters for real estate, even though buildings don't qualify

This is the part that most generic bonus-depreciation coverage tends to misstate. A building itself does not qualify for bonus depreciation. Residential rental property still depreciates over 27.5 years; commercial property over 39. Those recovery periods have not changed. So why does the OBBBA matter for private real estate investors at all?

Because a cost segregation study breaks the building apart for tax purposes.

When a property is acquired, a cost segregation engineer goes through the asset and reclassifies its components by IRS recovery class. The 27.5- or 39-year shell of the building stays where it is. But large chunks of value — typically anywhere from 15% to 30% of purchase price on a multifamily asset, sometimes more on industrial — get reclassified to 5-year, 7-year, or 15-year property. Carpet, cabinetry, appliances, specialized HVAC components, parking-lot improvements, fencing, signage, landscaping. None of those things are "the building." All of them now qualify for 100% bonus depreciation in the year placed in service.

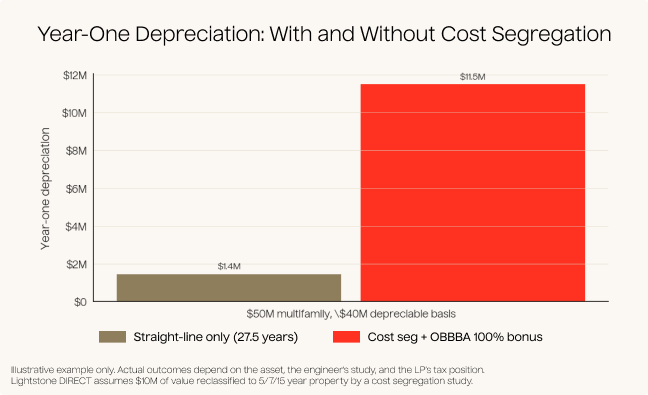

The combination is what produces the headline numbers. Without cost segregation, year-one depreciation on a $50M multifamily asset with $40M of depreciable basis is roughly $1.45M (straight-line, 27.5 years). With cost segregation that identifies, say, $10M of 5/7/15-year property, all of that $10M can be expensed in year one under the OBBBA. Year-one depreciation goes from roughly $1.45M to roughly $11.5M.

For an LP with a $250K position in that deal, the share of that year-one paper loss is meaningful. It generally flows through on a Schedule K-1, subject to passive activity loss rules. The deferred tax doesn't vanish — at sale, the depreciation gets recaptured at federal rates of up to 25% on the Section 1250 portion, and at ordinary rates on the Section 1245 personal property. But the LP has been given, in tax terms, what is essentialy an interest-free loan from the Treasury for the length of the hold.

The K-1 advantage, and why public REITs can't pass this through

This is the part of the bonus depreciation conversation that often gets skipped, and the one that matters most for choosing how to gain real estate exposure in the first place.

The accelerated depreciation deduction described above only reaches investors through a pass-through tax structure. Most private real estate syndications, including Lightstone DIRECT's single-asset deals, are partnerships, and partnerships pass their tax items through to partners on a Schedule K-1. The cost segregation deduction generated at the property level becomes a paper loss on the partner's K-1.

REITs do not work that way. A REIT — whether listed (AvalonBay, Equity Residential) or non-traded (BREIT, SREIT, Ares REIT) — is a corporation, and it pays distributions reported on Form 1099-DIV. The REIT itself can run a cost segregation study and accelerate its own depreciation; the deduction reduces the REIT's taxable income at the entity level. The deduction stops there. As a shareholder, you do not receive a share of the depreciation. You receive a dividend.

This is the central structural reason that two real estate investments yielding the same nominal cash return are not the same investment after tax. A 5% distribution on a partnership K-1, paired with a meaningful first-year depreciation loss, is taxed materially differently than a 5% REIT dividend taxed at ordinary income rates. (REIT ordinary dividends are not "qualified dividends" eligible for the preferential rate; the Section 199A pass-through deduction softens the bite somewhat, but does not replicate the depreciation flow-through.)

The OBBBA's restoration of 100% bonus depreciation widens this gap. Public-market real estate vehicles still pay no entity-level tax themselves, and still pay ordinary dividends to shareholders. Private partnership investors can now claim a substantially larger first-year paper loss against those same underlying assets. This tax efficiency comes with a structural tradeoff however. Public REITS offer daily liquidity, whereas private real estate is inherently illiquid and requires long-term holding periods. The same is true for direct ownership of investment real estate — a single landlord can also claim cost-seg-driven bonus depreciation — but in exchange for the tax efficiency, the landlord takes on all of the operational and credit risk of running a building. The K-1 syndication structure is the place where institutional management, single-asset transparency, and pass-through tax treatment all meet in one place.

Why we run cost segregation on every Lightstone deal

The math has always favored cost segregation on institutional real estate. Even at the pre-OBBBA 40% bonus depreciation rate, the present value of accelerated deductions vastly outweighs the cost of the engineering study (typically $10,000 to $25,000 on a single multifamily asset, less per-dollar at industrial scale). At 60% or 80% it was a no-brainer. At 100% it is something approaching malpractice not to do it.

Generally, every Lightstone DIRECT brings to accredited investors, multifamily or industrial, gets a full cost segregation study performed by experienced personnel.

The whiplash from 80% in 2023 down to 40% in early 2025 and back to 100% by mid-2025 is a useful reminder that tax policy is not, in fact, on a schedule. It is on a political calendar. The amount that flows through to investor K-1s has moved with the legislation. The utility of a cost segregation study remains the same.

The Caveats

Let's be a little careful. None of the above should drive a real estate investment decision in isolation. Three things worth holding alongside the headline.

Bonus depreciation is timing, not free money. When the property eventually sells, the depreciation is recaptured. The recapture rate — up to 25% federally on Section 1250 real property and ordinary income rates on Section 1245 personal property — means a portion of the benefit comes back at exit. The compounding value comes from holding the deferred tax for years, redeploying that capital, and, in some cases, using a 1031 exchange to roll the deferral forward, or a step-up in basis at death to convert deferral into elimination. For a four-year-hold investor with no estate plan and no intention of doing a 1031, the benefit is real, but smaller than the headline number suggests.

Passive activity loss rules still apply. Limited partners in private real estate generally generate passive losses. Passive losses can offset passive income, but not earned income, unless the investor qualifies as a real estate professional under Section 469. Most accredited investors are not real estate professionals and should not try to manufacture the status. The IRS audits manufactured claims aggressively. A larger paper loss does not change the rules that govern how it can be used.

Legislation can move again. The OBBBA "permanent" provisions are permanent in the sense that the law says so. Laws have been changed before. An investor building a multi-decade strategy on the assumption that 100% bonus depreciation will be available for every future deal in a portfolio is taking a political risk that most LPs underprice. The same political risk works the other way: a future Congress could extend full expensing to property classes that don't currently qualify, or expand the benefit in some other way. The point isn't direction. It's that the rate is something Congress turns.

What this changes about decision-making

The OBBBA didn't make a bad real estate deal a good one. It made a good real estate deal, held through the right structure, potentially much more tax-efficient than the public-market alternative.

For accredited investors weighing where to allocate capital to alternative assets, this gap is meaningful. It has always mattered, but the gap is wider now than it was a year ago.

Soren Godbersen is Chief Growth Officer at Lightstone DIRECT. This article is for informational purposes only and is not tax, legal, or investment advice. Tax outcomes depend on individual circumstances and on legislation that changes from year to year. Consult a qualified tax professional before acting on any of the above. Past performance does not guarantee future results; all investments carry risk. The mathematical examples provided are strictly hypothetical and do not represent the actual performance, underwriting, or tax outcomes of any specific past or future investment.

Further reading:

- One, Big, Beautiful Bill provisions (IRS overview of all OBBBA tax provisions).

- Treasury and IRS guidance on the additional first-year depreciation deduction under the OBBBA (Notice 2026-11).

- Internal Revenue Code Section 168(k) (additional first-year depreciation), Section 1250 (depreciation recapture on real property), Section 1245 (recapture on personal property), and Section 469 (passive activity loss rules).

- Public Law 119-21 (One, Big, Beautiful Bill Act of 2025).

Soren Godbersen

Soren Godbersen is Chief Growth Officer at Lightstone DIRECT, where he oversees investor experience, day-to-day operations, marketing, and strategic direction of the group. Previously Godbersen was Chief Growth Officer at EquityMultiple, a category-defining real estate investment platform for accredited investors where he led the Marketing and Investor Relations Teams, helping to grow the firm’s AUM to nearly $1B, and investor network to over 5,000 individual high-net-worth investors. Godbersen holds a Bachelor's of Arts in Economics with Honors from Whitman College.