Tax Efficient Real Estate Investing

Introduction

One of the main advantages of investing in real estate is its ability to generate a strong income stream while being extremely tax efficient. For many high-net-worth investors, taxes can significantly erode portfolio performance, meaning the true after-tax yield on traditional investments is often far lower than the headline return once taxes are applied.

For limited partners (LPs) in private real estate syndications, these tax advantages are a significant determinant of how much investment income is actually kept. Tools like depreciation allow investors to reduce their taxable income and defer a portion of what they owe, often paying at lower rates when gains are realized. This tax deferral allows investors to postpone paying taxes on their income until the property is sold, allowing for stronger after-tax returns and long-term growth that few other asset classes can match.

At the end of the day, it’s not just about what you earn — it’s about what you keep.

What is Depreciation?

Depreciation refers to the gradual write-off of a building’s value over its useful life, accounting for wear and tear while the property continues to generate income. While depreciation reflects the natural aging of a building, it’s important to view it in context. Yes, a property gets older over time, but for most well-located and well-managed assets, appreciation in land value and rental income growth more than offset that aging effect. In practice, the tax advantages of depreciation generally outweigh the economic cost, allowing investors to benefit from meaningful annual deductions while the property continues to generate stable, and often growing, income.

To be eligible for depreciation, a property must be held for income-producing purposes, be held for more than a year, and have a determinable useful life. Residential properties are depreciated over 27.5 years, while commercial properties are depreciated over 39.

Depreciation doesn’t remove taxes — it simply defers them until the property is sold, which allows investors to keep more of their cash distributions throughout the hold. By lowering taxable income each year, investors retain more of their distributions instead of paying them out immediately. When those deferred taxes are eventually paid, they’re taxed at the depreciation recapture rate of up to 25% rather than the ordinary income rate of up to 37%, allowing for enhanced after-tax returns.

Basis and Its Role in Tax Efficiency

The cost basis of a property refers to the total amount spent to acquire the asset and prepare it for use, and includes things such as title costs, legal fees, and capital improvements. Since land is assumed to have an indefinite useful life and therefore isn’t depreciable, it is excluded to calculate the depreciable basis, which is the portion of the investment that qualifies for annual depreciation deductions. This is adjusted over time, with depreciation reducing it and capital improvements adding to it. This yields the adjusted basis that determines the taxable gain when the property is sold.

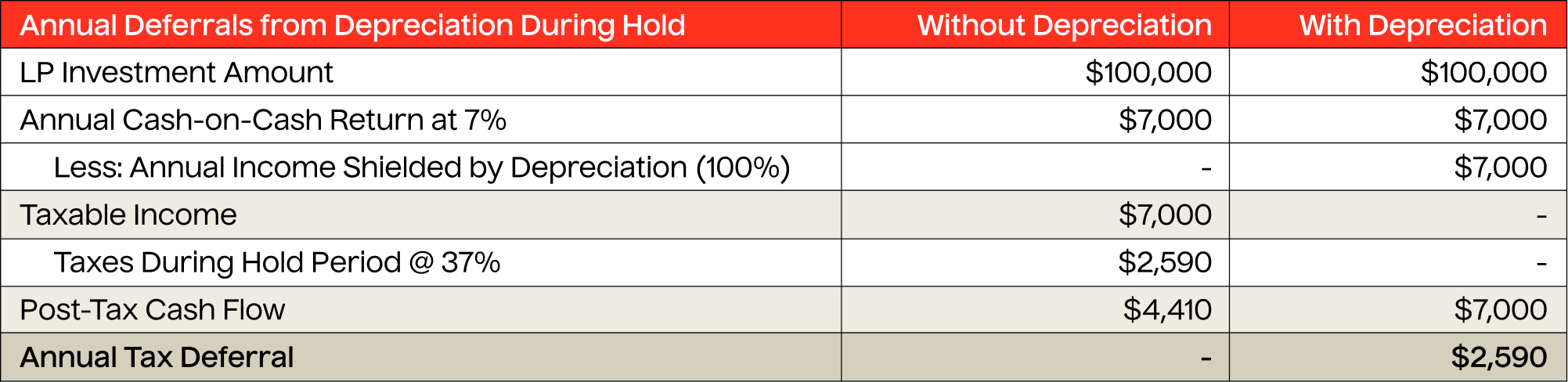

For example, assume a GP acquires an industrial property for $5 million, with $1 million allocated to land and $4 million to the building. An LP investing $100,000 earns a 7% annual cash-on-cash return, or $7,000 per year. Assuming depreciation fully shields the property’s income during the hold, the investor can defer $2,590 in taxes annually, to be taxed upon sale at a 25% rate as opposed to the ordinary tax rate of 37% in the same year.

Accelerating Deductions with Cost Segregation and Bonus Depreciation

Typically, depreciation is spread evenly over the life of the building’s useful life. However, sponsors are able to speed up those deductions through cost segregation. This involves hiring an engineering firm to identify individual parts of a property, such as flooring, landscaping, or parking areas, which can be depreciated over shorter periods. Front-loading these deductions allows more of the tax benefits to apply in earlier years, which improves cash flow without changing the property’s actual performance. This also has the ability to generate passive losses, which investors can use to offset other passive income within their portfolio.

The Tax Cuts and Jobs Act expanded this strategy with bonus depreciation, which lets sponsors write off qualifying assets immediately in the year they’re placed in service. While this benefit began phasing down in 2023, the One Big Beautiful Bill Act reinstated full 100 percent bonus depreciation for most qualifying properties in 2025.

Accelerating deductions in this way can significantly improve tax efficiency by capturing more of the available benefits upfront to offset income in the early years of the investment. While this reduces the remaining depreciable basis, and therefore limits future depreciation, it doesn’t eliminate the advantage altogether. Excess losses can generally be carried forward, allowing investors to apply them against future years’ income.

Depreciation and the Tax Implications of a Sale

When an investment property is sold, depreciation doesn’t disappear - it simply affects how the gain is taxed. Over time, depreciation reduces the property’s adjusted basis, which increases the gain recognized at sale. The portion of income that was sheltered by depreciation during the hold is recaptured at sale and taxed at a maximum federal rate of 25%, instead of the higher 37% ordinary income rate that would have applied if it were taxed annually. The remaining profit — the true gain on sale — is taxed at the long-term capital gains rate of 23.8% (including the net investment income rate).

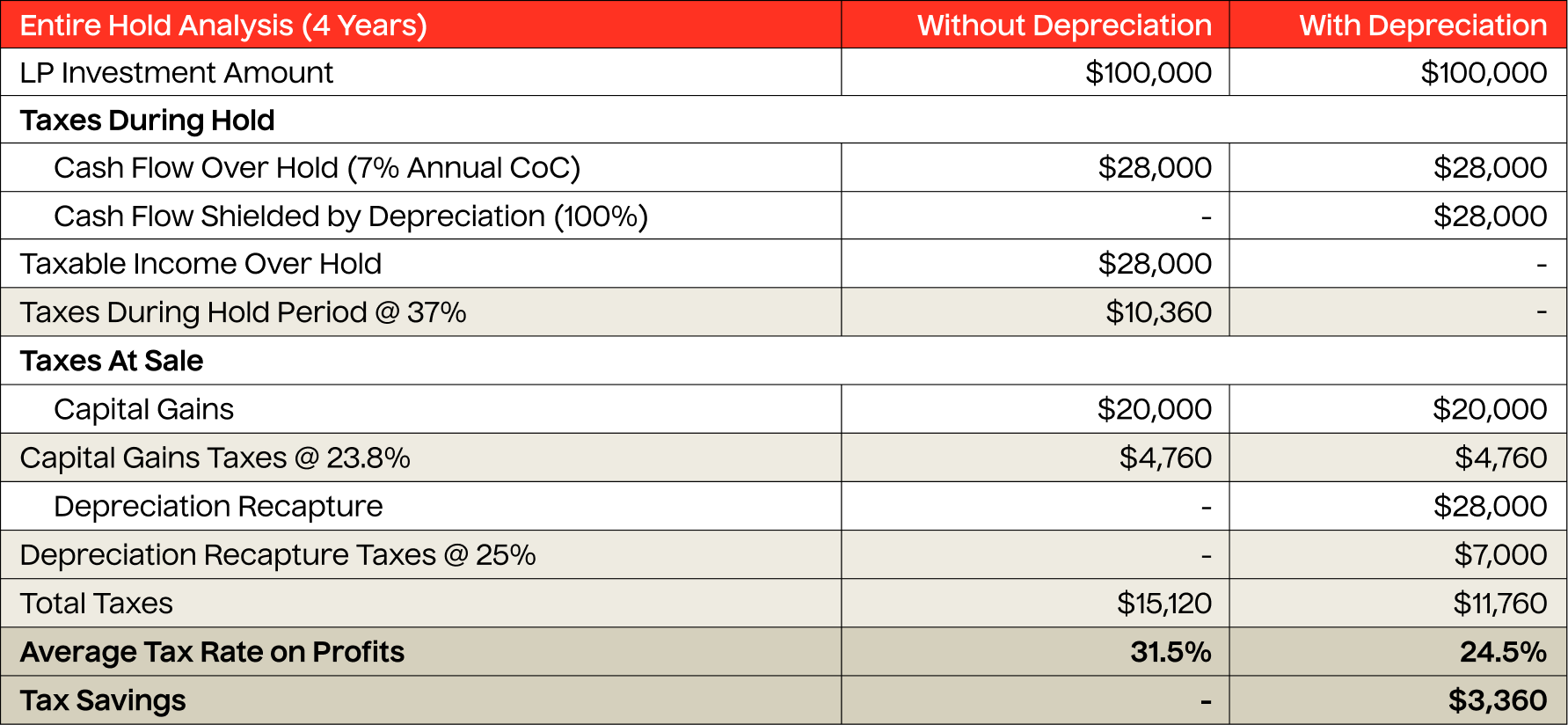

This creates a clear tax deferral advantage. For example, an LP investing $100,000 in a property earning a 7% annual return over a four-year hold would pay $15,120 in total taxes without depreciation. With depreciation and later recapture, that total drops to $11,760, which yields $3,360 in savings. The deferred taxes are still paid upon sale, but at lower recapture rates instead of higher ordinary income rates, which allows investors to keep more of their earnings working throughout the investment.

The Benefits of Tax-Equivalent Yield

Tax-equivalent yield is a prime illustration of how private real estate’s tax efficiency can significantly enhance after-tax returns. Because a notable portion of real estate distributions are often sheltered by depreciation and other deductions, investors are able to retain more of their income than they would from other investment vehicles.

For instance, a 7% cash-on-cash return which is fully sheltered by depreciation would deliver the same after-tax income as a taxable investment yielding roughly 11%, assuming a 37% marginal tax rate. This allows investors to achieve comparable after-tax results while taking on less risk. Evaluating returns through a tax-equivalent lens helps demonstrate the true power of tax-efficient income, highlighting not just what’s earned, but what’s ultimately kept.

The Bottom Line

Tax efficiency is one of the biggest strengths of private real estate investments. Beyond income and appreciation, its structure offers advantages few other investments can match: tax benefits like depreciation that allow income to be sheltered and deferred, accelerated deductions that improve early cash flow, and lower rates that enhance returns and reduce the burden when gains are realized. These factors make it one of the most effective long-term vehicles for building and preserving wealth.

Annina Vaisanen

Annina Vaisanen is part of the Investor Relations team at Lightstone DIRECT, where she focuses on coordinating and enhancing the investor experience across the platform. In addition to overseeing investor relationships, she also plays a key role in streamlining systems and processes that support efficient operations across the group.