LP vs. GP: How Co-Investment Aligns Interests in Direct Real Estate Deals

Partnership. It is core to private real estate investing, both in spirit and in terms of legal structure. Fundamentally, a JV (joint venture) real estate investment consists of two primary entities: Limited Partners (LPs) and General Partners (GPs).

This article will:

- Recap the basic definitions of Limited Partners (LPs) and General Partners (GPs) in private real estate transactions

- Cover the typical dynamics of the LP / GP relationship

- Offer thoughts on how the right model can bring alignment to LPs and GPs, creating partnership in the truer sense of the word.

Lightstone, as the GP (general partner) invests 20%+ of the equity in each Lightstone DIRECT deal, ensuring a rare level of alignment with individual LP (limited partner) investors.

Most readers will likely recognize these terms, but let’s take a moment for some basic definitions.

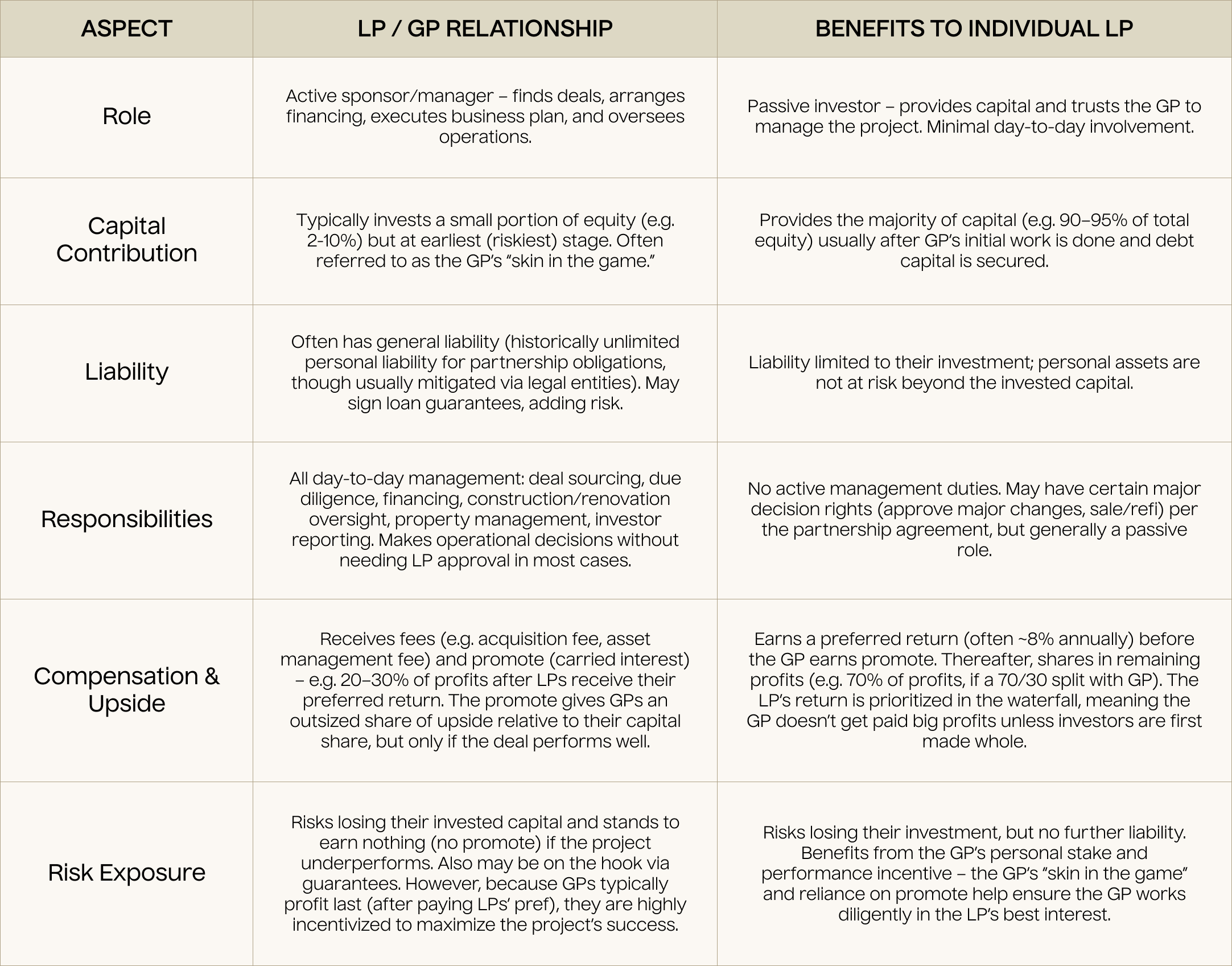

LPs (limited partners in real estate deals) are the passive investors who contribute the bulk of the capital to a real estate deal, while GPs (often called sponsors) are the active managers who source, execute, and oversee the investment. In a typical limited partnership real estate deal, LPs might provide 80%–95% of the equity, with GPs contributing the remaining 5%–20%[1][2]. LP investors generally appreciate “skin in the game” — the GP investor staking a significant amount of capital in the equity of the deal.

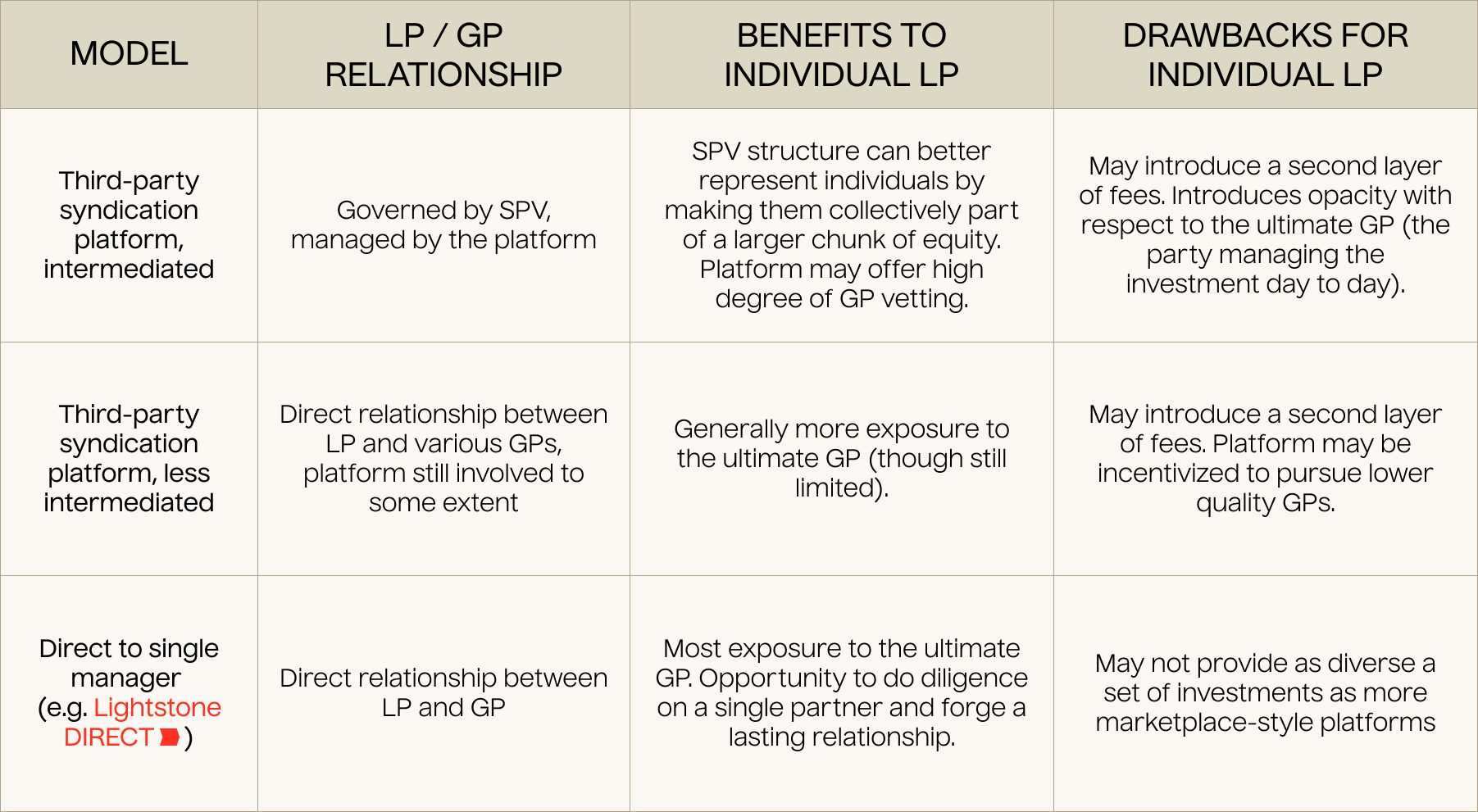

However, many GPs will co-invest a relatively small amount — often less than 5%. Online real estate investing platforms generally fall within one of three models. In some cases, individual LPs will be consolidated into a single SPV (single purpose vehicle), with a managing entity acting as a go-between with respect to the GP (or “sponsor”) and each individual LP investor. In other cases, individual LPs will deal directly with sponsors. In the case of a “marketplace”-style investment platform, though, individual LPs would bear the same relationship with the GP, but would be a layer removed, with the intermediating platform still taking fees in many cases.

General Partner vs. Limited Partner: Roles and Responsibilities

At a high level, you can think of the GP / LP dynamic as active management vs. passive ownership:

General Partner (GP): The GP (or sponsor) is the active manager of the deal. Over the span of a given private-market real estate deal, they will take on all of these responsibilities:

- Acquisition: They find the property via an auction platform, brokerage, word-of-mouth relationship, or preexisting network. Once an opportunity is identified, the GP will underwrite the property, arrange financing, handle legal structuring, and work through the closing process. Securing favorable funding will depend on the GP’s creditworthiness, capital market’s relationships, and ability to present a cogent business plan, qualitatively and quantitatively.

- Execution of the business plan: Depending on the strategy, the GP may execute on development, varying degrees of capital improvements, a leasing strategy, or even aggressive repositioning, like converting a central business district office into workforce housing. Irrespective of the strategy, the GP is responsible for managing the investments finances, keeping costs in line with the original pro forma and pursuing rental income at or above the business plan’s forecast.

- Disposition: The GP will look to exit the investment at a favorable moment, given supply/demand dynamics in the local market; more general macroeconomic conditions and the interest rate environment; and the present state of the property and rent roll vs. the GPs original basis [4][5]. Knowing how to navigate the sales process, and identify the right buyer profile, is a hallmark of successful GPs

The GP typically invests some of their own money (often 2-10% of the equity) and often signs on loans or guarantees — meaning they’re in from the start, when risk is highest[2]. This “skin in the game” varies substantially, and savvy LP investors will prefer a great co-investment from the GP, demonstrating greater conviction in the deal and alignment of interest. The GP’s profit share is usually disproportionate to their small equity contribution — for example, a GP might contribute 10% of the capital but receive 20–30% of the upside — reflecting the value of their expertise and effort[6].

Lightstone, as an institutional-scale GP, commits a minimum of 20% of the equity in each Lightstone DIRECT investment. This demonstrates conviction in the deal and ensures alignment with individual LP investors. This relatively large co-investment also reflects scale: many smaller GPs must assume higher leverage and contribute less equity in order to execute on a multi-unit property. Lightstone, by contrast, has the balance sheet to comfortably co-invest well over 20% in each deal. Put differently, these are deals that Lightstone would be doing anyway, with or without LP involvement.

Limited Partner (LP): The LPs are the passive investors who provide the majority of the capital (often 90–95% of the equity)[7]. An LP’s role is largely hands-off — they rely on the GP’s experience to manage the investment. LPs have limited liability (hence the name), meaning their risk is capped at their invested amount[3]. In some cases, institutional LPs may have veto rights (for instance, approving a sale or a refinancing, depending on the partnership agreement[8][9]). Individual LPs (such as investors in Lightstone DIRECT) typically do not have voting rights — this is not necessarily a bad thing; it means that major decisions are left to real estate professionals who are close to the investment.

In return for contributing passive capital, LPs receive a priority in the cash flows — typically a preferred return on their investment (often around 6–10% annually) and then a share of the remaining profits. This preferred return is subordinate to debt and any more senior tranches of capital. LPs’ upside is somewhat capped by the fact that the GP takes a promote, but most waterfall structures are designed to ensure LPs are paid first and adequately. For example, a 7-8% preferred return is common, after which remaining profits might be split 70% to LPs and 30% to the GP[10]. This structure is meant to de-risk the investment for LPs while still rewarding GPs for strong performance[11][12].

The table below summarizes the key differences between GPs and LPs in real estate partnerships:

Aligning Interests Through Structure and Co-Investment

When GPs and LPs win (and lose) together, the GP is motivated toward long-term value creation over short-term gains[17]. But how is alignment achieved in practice? Two primary mechanisms do the heavy lifting: the economic structure of the deal (profit sharing arrangements) and the GP’s co-investment (skin in the game).

1. Performance-Based Compensation (Waterfall Structure). Real estate partnerships use a waterfall distribution model to allocate cash flows. This typically gives LPs priority — for example, the partnership will distribute available cash such that LPs receive their full preferred return (and often their capital back) before the GP earns a share of profits[18][19]. Only after LPs are made whole does the GP start to earn its promote (a favorable percentage of the profits). This means the GP cannot make a big profit unless the investors do well, which naturally aligns the GP’s motivation with LPs’ interests. A common profit split might be 70/30 (70% to LPs, 30% to GP) after an 8% preferred return (or “pref”) possibly with higher GP splits if returns exceed certain hurdles (e.g. 50/50 if returns are extremely strong)[10]. In many cases, the GP’s promote structure will be more favorable for development deals, or more complex value-add strategies or repositionings, where the GP is taking on more risk and uncertainty.

Note: while the terms may change from deal to deal, Lightstone DIRECT will most often structure deals as follows:

- An 8% preferred return to LPs

- A 80/20 spit above the 8% hurdle

- All returns to LP investors presented net of promote and fees

The key is that the GP’s upside is pegged to performance — if the deal underperforms, the GP’s share shrinks or disappears. As a result, GPs work hard to maximize returns for everyone, since their “carry” (promote) depends on it. In short, the waterfall structure aligns interests by rewarding the GP for success and protecting the LP on the downside. A properly structured waterfall is critical for investor-sponsor alignment, ensuring the sponsor only profits after meeting investor return thresholds [18][20].

2. GP Co-Investment (“Skin in the Game”). Beyond a well-calibrated waterfall structure, nothing aligns a sponsor with investors quite like having a significant amount of their own capital at stake. When a GP contributes significant capital alongside the LPs, it sends a powerful message: the GP truly believes in the project — if the investment performs well, the GP will win alongside individual LPs; if it underperforms, the GP will feel pain alongside LP investors. Many institutional LPs mandate that sponsors put in a meaningful share of the equity (often around 5–10% or more) for precisely this reason[21][22]. Individual LP investors, however, may not know to look for this form of alignment in deal docs. In practice, even a ~10% co-investment by a GP is considered strong alignment in most deals[22]. But why stop there? Lightstone commits at least 20% of the equity in each Lightstone DIRECT investment, creating a degree of alignment that is rare in the space.

On the other hand, a red flag for LPs is a sponsor who contributes little to no equity of their own while charging high fees[24]. If a deal is “fee-heavy” (e.g. big acquisition fees, asset management fees, etc.) and the GP has only a token investment, the GP might profit simply from doing the transaction, with their own returns depending less on long-term performance[24]. In such misaligned scenarios, the GP’s incentive skews toward closing more deals (to collect fees) and stretching their own equity thin across multiple transactions, rather than committing significant “skin in the game” and sharing in the outcome with LPs. If a GP stands to earn a relatively high percentage of their profits on up-front fees, they may lack proper incentive to generate long-term value and maximize long-term returns on behalf of LP investors. Proper alignment demands both reasonable, performance-weighted fees and a meaningful GP co-investment so that the sponsor’s interests are wholly tied to the deal’s outcome[16][26].

Waterfall structure and GP co-investment are two of the most important things to consider for any self-directed investor considering a private-market real estate investment. Be sure to find this information in the PPM and consider how aligned the GP’s interests are with your own, per these structures.

Why Alignment Matters More Than Ever in 2025

It’s worth framing this discussion in the context of 2025’s real estate capital markets. The past few years have been turbulent for real estate investors: a pandemic, inflation, and rapid interest rate hikes, and even some high-profile stumbles in the real estate crowdfunding space. Many investors have grown more cautious and discerning about where they put their money.

For example, early 2025 began with cautious optimism in real estate after a period of sluggish fundraising and declining property values amid market volatility[27]. But fresh uncertainties (like trade policy shocks and persistently high interest rates) tempered that optimism, reminding investors that the halcyon days of pre-2022 may not be coming back soon [27]. In such an environment, investors are more likely to favor deals backed by experienced, well-aligned, well-capitalized GPs. Indeed, today’s accredited investors have become keenly aware of alignment: many feel burned by the “overpromise, underdeliver” approach of some online syndication platforms in the late 2010s. The result is a flight to quality — investors now demand transparency, realistic projections, and true alignment of interests from sponsors.

A recent CBRE survey found that elevated financing costs and volatility are top concerns for investors, who are nonetheless eager to deploy capital in the right opportunities[30][31]. With tighter margins, there is simply less room for error or misalignment. LPs want to ensure GPs have “skin in the game” and shared risk, so that deals are underwritten conservatively and managed diligently. In short, alignment isn’t just a feel-good concept — it’s a practical risk mitigation strategy, especially in a market where the cost of capital is high and not every deal will be a homerun. As one real estate investment group observes, when interests are aligned, “investment decisions prioritize long-term success, LPs get fair compensation before sponsors profit, and sponsors focus on performance, not upfront fees”[32][25]. Our perception, both anecdotally from conversations with LPs and from such research: individual LPs have rightly grown discerning about the structure of online syndications and the GPs behind them.

Lightstone DIRECT’s 20% Co-Investment: A Case Study in Alignment

A cornerstone of Lightstone DIRECT’s model is its significant co-investment in every deal — Lightstone commits 20% or more of the equity in each offering. This level of commitment is far above industry norms (in our surveying of similarly sized or smaller GPs, mid-single-digit percentage of equity is common)[21]. In Lightstone’s case, the company is essentially saying: “For every deal, we’re putting our money where our mouth is — at least 20% of it.” Such a substantial co-investment ensures “true skin in the game,” materially aligning the GP and LP interests from day one. If you invest alongside Lightstone, you know the GP stands to benefit only if you benefit, and that they have serious capital at risk right alongside yours. One simple way to look at it: these are investments that Lightstone would make with or without the capital of individual LPs.

In terms of alignment with individual LPs, Lightstone DIRECT does not stop there. Because individual LPs invest directly with the GP (Lightstone), there are no intermediary crowdfunding portals or extra layers of middlemen in between. This means fees may be more transparent and there’s only a single layer of promote — you’re not paying a platform an extra cut, and the GP isn’t sharing its promote with third parties. Lightstone’s fee structure is simplified and performance-centric: the GP’s profit potential comes primarily from a) performance of the underlying investment (as Lightstone is staking 20%+ of the equity) and the promote (performance-based profits), rather than from a stack of front-loaded fees.

In a GP / LP relationship, “partnership” is not purely about the economics. Lightstone DIRECT strives to foster a direct relationship with investors in a way that typical syndication platforms do not. Investors on the platform are treated as true partners — each investor is connected with a dedicated point of contact from our Capital Formation Team, and no one is relegated to a mere number in a ticket queue. Because there’s no intermediary, Lightstone as GP is fully accountable to its LPs. We, as the manager, must look individual investors in the eye and deliver. The direct nature of the platform means investors can diligence the GP (Lightstone) and then choose deals on a one-by-one basis, rather than being tied up in a blind fund or aggregator. The vertically integrated nature of Lightstone means that individual LPs are closer to all facets of the investment — with acquisitions, asset management, and property management within a single firm, Lightstone is able to offer individual LPs a high degree of visibility into the progression of the business plan for each investment.

All of these factors work in concert to ensure that LPs and the GP are rowing in the same direction:

- Substantial GP capital at risk

- Direct investor access to the sponsor

- Transparent fees

- Alignment of profit potential between GP and LPs

Lightstone DIRECT brings individual LPs a partnership mentality; we seek to create lasting relationships with each and every LP and align our interests across a series of single-asset transactions, rather than just treating investors as a source of fees.

Conclusion

In the world of general partner vs. limited partner real estate investing, thoughtful structuring and co-investment go a long way toward creating a win-win scenario. When GPs have meaningful skin in the game and only earn outsized rewards after LPs are taken care of, the classic potential conflicts between “the money” (LPs) and “the manager” (GP) largely fall away.

As we’ve discussed, mechanisms like preferred returns, promotes tied to performance, and GP co-investment ensure that all parties’ incentives are calibrated for collective success. In the current real estate climate, with investors more selective and market conditions still demanding caution, such alignment has gone from a nice-to-have to critical.

As an individual LP considering a private-market real estate investment, closely consider the structure of the deal (profit sharing, fees, and sponsor co-investment). If your GP does not feel like a partner, in all senses of the word, look elsewhere.

[1] [2] [3] [4] [5] [6] [7] [8] [9] [14] How To Master GP Vs LP Real Estate Partnerships: A Plain-English Guide | Primior Group https://primior.com/how-to-master-gp-vs-lp-real-estate-partnerships-a-plain-english-guide/

[10] [11] [12] [13] [15] [16] [17] [18] [19] [20] [22] [24] [25] [26] [32] Alignment of Interests in Real Estate Investing is Critical: How Seize Returns with Shared Goals - Piping Rock Partners https://prpi.com/investor-sponsor-alignment-in-real-estate-investing/

[21] [23] Private Real Estate Equity: The Hidden Power Of Co-GP Structures In 2025 | Primior Group https://primior.com/private-real-estate-equity-the-hidden-power-of-co-gp-structures-in-2025/

[27] 2025 Midyear Outlook | Blue Owl Capital https://www.blueowl.com/insights/2025-midyear-outlook

[30] [31] 2025 U.S. Investor Intentions Survey: Investment Activity Poised for Growth | CBRE https://www.cbre.com/insights/briefs/2025-us-investor-intentions-survey

Soren Godbersen

Soren Godbersen is Chief Growth Officer at Lightstone DIRECT, where he oversees investor experience, day-to-day operations, marketing, and strategic direction of the group. Previously Godbersen was Chief Growth Officer at EquityMultiple, a category-defining real estate investment platform for accredited investors where he led the Marketing and Investor Relations Teams, helping to grow the firm’s AUM to nearly $1B, and investor network to over 5,000 individual high-net-worth investors. Godbersen holds a Bachelor's of Arts in Economics with Honors from Whitman College.