Learn more about everything Lightstone DIRECT has to offer

Generating magic link...

Why Meaningful GP Co-Investment Matters More Than Ever

Alignment, downside protection, and institutional discipline in private real estate

In private real estate, true alignment between LPs and GPs is easy to talk about and surprisingly rare to find. Nearly every sponsor claims to be “investor-aligned,” yet in practice many managers commit little or no meaningful capital alongside their limited partners. From the sponsor’s perspective, the incentives may be skewed far toward making revenue on fees, rather than maximizing risk-adjusted returns on behalf of LPs. This lack of alignment may get worse in the case of a “marketplace”-style platform, where a crowdfunding platform is collecting a further layer of fees and responding to its own set of incentives.

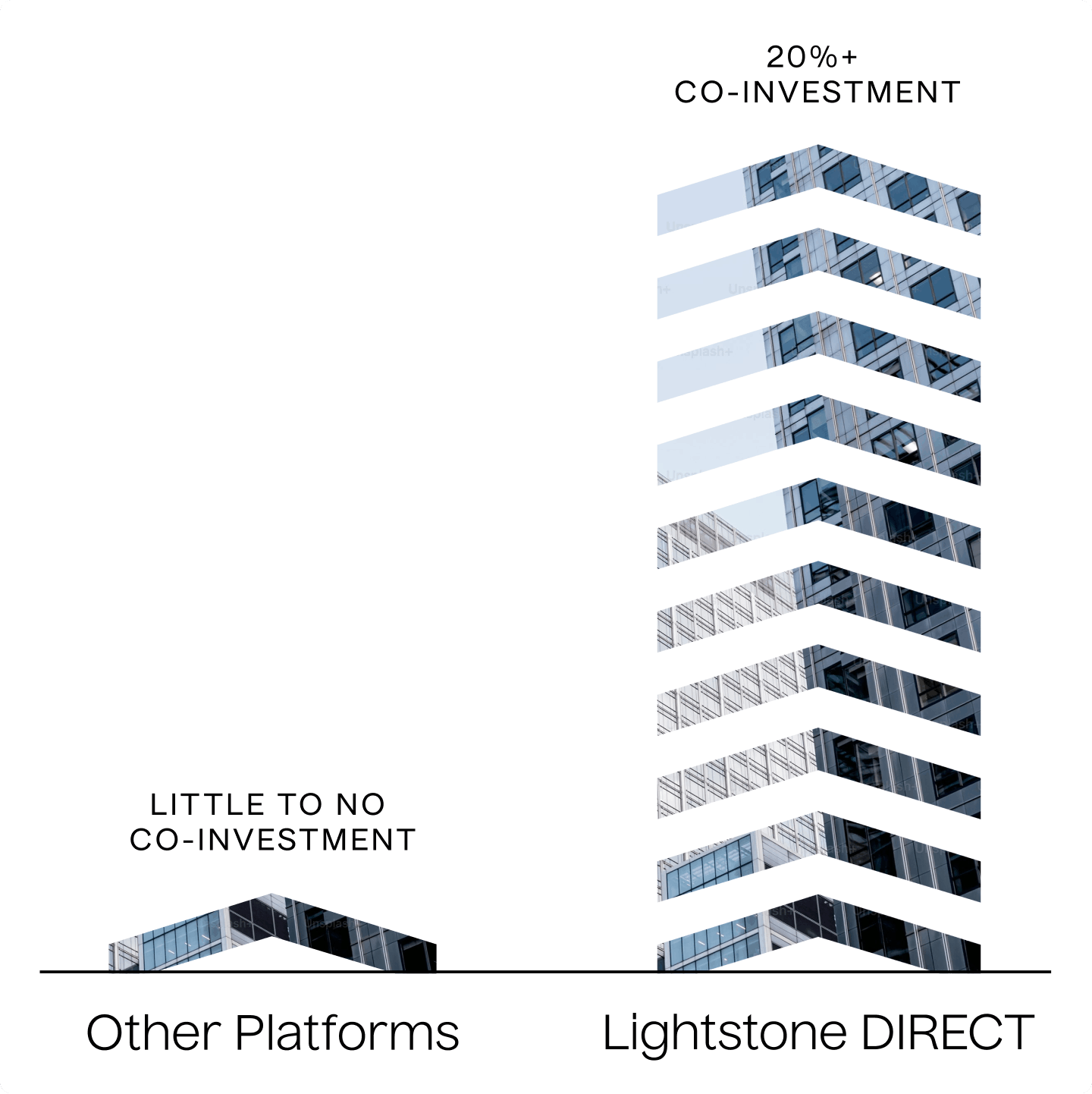

Lightstone DIRECT is built differently: the opportunities on Lightstone DIRECT are the same multifamily and industrial opportunities that Lightstone pursues with its own capital. For that reason, Lightstone commits at least 20% of the total equity in every investment offered on the platform—alongside individual accredited investors, bearing the same set of risks and incentives. This is not token participation. It is substantial, at-risk capital deployed from Lightstone’s own balance sheet.

This level of co-investment materially exceeds industry norms, where sponsor commitments are often in the low single digits—or entirely absent. More importantly, it can change how decisions are made across the full lifecycle of an investment, from underwriting through exit.

The misalignment problem in platform-based private real estate investing

Over the past decade, access to private real estate has expanded dramatically. Technology platforms, aggregators, and semi-liquid vehicles have lowered minimums and increased deal flow for individual investors. While this trend has improved accessibility, it has not consistently improved alignment.

In many structures, sponsors are incentivized to:

- Prioritize transaction velocity over selectivity

- Lean on optimistic underwriting to support fundraising

- Favor fee stability over long-term asset optimization

- Accept asymmetric risk where LPs absorb downside while GPs retain optionality

These dynamics tend to surface most clearly during periods of market stress. When valuations reset, liquidity tightens, or leasing assumptions fall short, the true incentive structure of a deal is revealed. Misalignment was on full display in the period following mid-2022, when interest rates rose quickly. Sponsors who made overly aggressive use of leverage, or who relied on overly rosy underwriting at the tail end of bull run, left individual LPs in the lurch in a number of high-profile cases.

Capital that was lightly committed is easily walked away from. A meaningful GP co-investment puts the onus on the manager to earn a relatively higher percentage of profits from asset performance rather than fee load.

Lightstone’s approach explicitly rejects this asymmetry. This is why Lightstone invests, at minimum, 20% of the equity in each Lightstone DIRECT deal you see. These are the same investments Lightstone pursues on its own balance sheet.

What 20% co-investment actually changes

A 20% GP commitment is not window dressing—this degree of co-investment materially changes the set of incentives that we, Lightstone, operate under. Lightstone DIRECT is a committed steward of capital, and committed to providing an elevated investor experience on all fronts. That said, this co-investment imposes hard-and-fast incentive alignment that should help any individual investor sleep easier. This takes shape across four critical dimensions of the investment process.

1. Underwriting standards become non-negotiable

When a sponsor is underwriting with only marginal capital at risk, marginal deals can slip through. When a sponsor is underwriting with tens of millions of dollars of its own equity at stake, the tolerance for overly aggressive assumptions collapses.

At Lightstone, every investment must clear the same internal vetting process and investment committee scrutiny that govern the firm’s wholly owned balance-sheet investments (the investments with no LP capital in play). This uniform process includes conservative exit assumptions, multiple layers of due diligence, stress-tested debt structures, robust sensitivity analysis, and a bias toward durable in-place cash flow rather than speculative appreciation.

This discipline has been forged across multiple market cycles. Since its founding in 1986, Lightstone has invested through recessions, rate shocks, and demand dislocations—experience that informs both what the firm pursues and what it avoids. The firm’s acquisition process follows a creative but measured approach – acquisitions personnel seek off-market assets and against-the-grain strategies, but each opportunity (including all opportunities evaluated for Lightstone DIRECT) must pass vetting of asset management and the executive team.

2. Capital structure decisions favor resilience, not fragility

Leverage is one of the most powerful tools in real estate investing, and a unique facet of the asset class. It also introduces risk, especially for less experienced operators. Sponsors with limited capital at risk may be incentivized to maximize leverage to amplify IRRs, even when doing so increases refinancing or maturity risk.

Meaningful co-investment changes that calculus. Lightstone’s capital sits in the same position as its investors’ capital, exposed to the same debt terms, covenants, and duration risk. As a result, the firm emphasizes:

- Moderate leverage levels

- Fixed-rate or well-hedged floating-rate exposure

- Flexibility to hold through dislocated markets

This approach has proven especially valuable in the current environment, where interest rates have reset higher and capital markets have become more discriminating. Properties with resilient capital structures have retained optionality; those without have not.

3. Asset management decisions optimize long-term value, not short-term optics

Once a deal closes, boots-on-the-ground operations drive outcomes. Leasing strategy, capital allocation, expense management, and tenant selection all shape outcomes over time.

When the GP’s capital is meaningfully at risk, asset management becomes less about near-term mark-ups and more about creating durable value. That means:

- Investing in capital improvements that enhance tenant retention

- Tightly controlling cost

- Understanding the mindset and demand dynamics of the typical tenant, specific to the asset subtype and geographic location.

Because Lightstone is vertically integrated—handling acquisitions, asset management, and property management in-house—it has direct control over these decisions. Co-investment ensures that this control is exercised in direct alignment with LP outcomes, not in tension with them.

4. Exit timing is governed by market reality, not platform needs

In lightly aligned structures, exits can be driven by factors unrelated to asset fundamentals: fund life constraints, liquidity promises, or the need to demonstrate realized performance for marketing purposes.

With 20% of the equity at risk, Lightstone has no incentive to force an exit that compromises value. The firm can hold when markets are dislocated and transact when pricing appropriately reflects intrinsic value.

This flexibility is particularly important in single-asset investments, where timing can materially affect outcomes. Lightstone DIRECT’s deal-by-deal structure allows investors to get comfortable with individual opportunities without exposure to forced portfolio-level decisions common in pooled vehicles.

Why GP “skin in the game” matters in today’s market

The current real estate cycle is characterized by dispersion across markets, asset classes, and vintages. Pricing has reset unevenly, operating fundamentals vary widely by asset class and geography, and capital is no longer indiscriminately available.

In this environment, manager quality and incentive alignment matter more than beta exposure. Returns are increasingly driven by:

- Asset selection rather than a generally rising tide

- Operational execution rather than financial engineering

- Balance sheet strength rather than leverage tolerance

Alignment you can quantify

Unlike more abstract claims of “skin in the game,” Lightstone’s commitment is measurable and contractual. In each investment:

- Lightstone invests a minimum of 20% of total equity

- Capital is contributed on the same terms as LP capital

- Deal performance makes up a larger share of Lightstone’s overall returns for a given deal, rather than fees earned from LPs.

- Losses, should they occur, would be shared proportionally

This structure ensures that success is mutual and failure is not externalized. It also explains why Lightstone can be selective in what it offers. When every deal requires substantial internal capital, selectivity is unavoidable—and beneficial.

A partnership, not a platform

Lightstone DIRECT was not designed to maximize deal flow, nor was it created to expand the universe of deals that Lightstone can, or will, do. We built this platform to extend access to a proven institutional platform while preserving the investment discipline that has made Lightstone successful for four decades.

Meaningful co-investment is the clearest expression of this mission. As an individual investor, this should give you full faith that we have confidence in each deal you see.

In private real estate, trust is earned not through words, but through performance, and the reasonable sharing of risk. Lightstone’s 20% co-investment ensures that every decision is made with the same question in mind:

Would we make this investment if we were the only equity in the deal?

The answer, in all cases, is yes.