Why Targeting Class B Might Be a Smarter Play Today: Understanding Class A, B, and C Multifamily Real Estate

Introduction: The Real Case for Class B Multifamily Real Estate

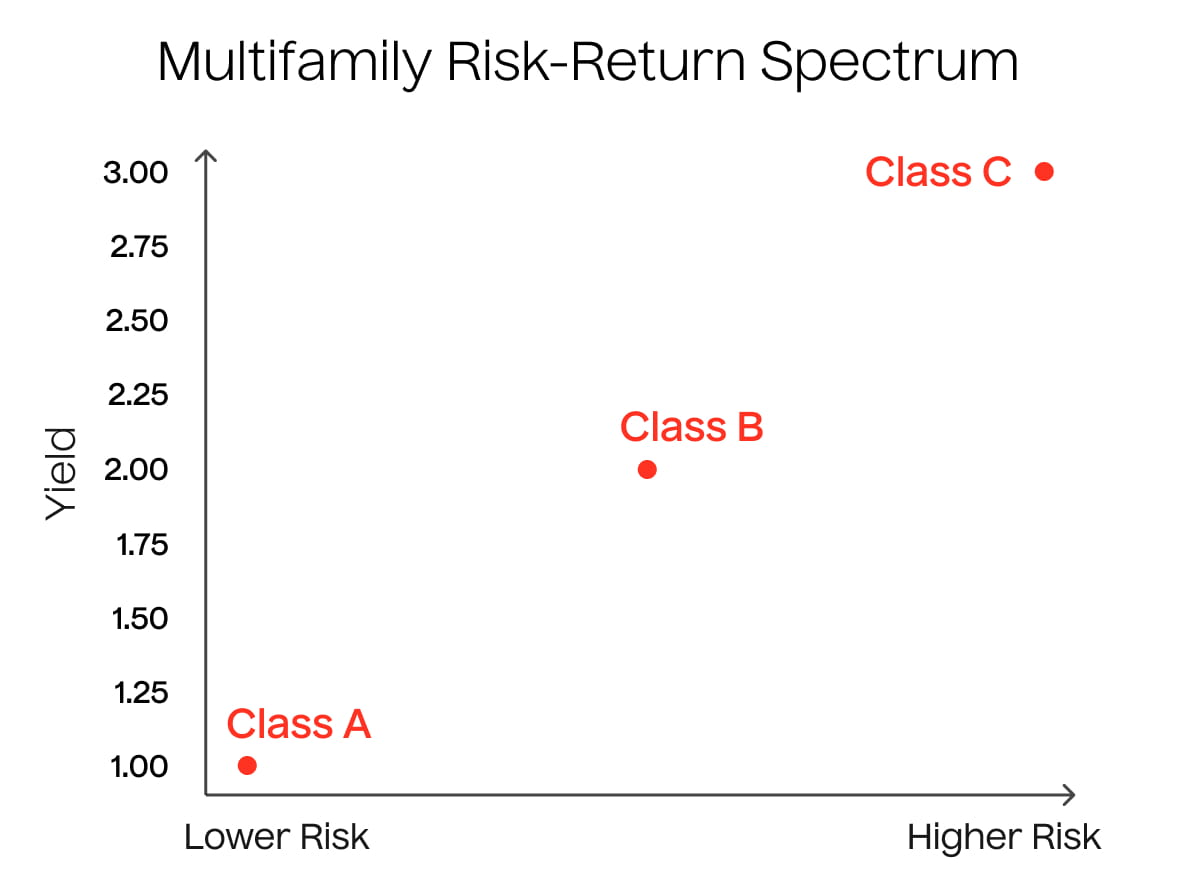

In today’s market, Class B multifamily real estate represents the most attractive balance between yield, risk, and tenant demand. While investors chasing Class A often pay for prestige at the expense of returns, and Class C assets can expose portfolios to volatility and CapEx surprises, Class B sits in the optimal risk-adjusted segment of the market.

As we enter 2026, this balance is more critical than ever. A period of cyclical dislocation driven by elevated interest rates and a historic supply wave in luxury apartments is beginning to clear, revealing a landscape where Class B assets are positioned to outperform. At Lightstone, we have built one of the nation’s largest privately held multifamily portfolios by focusing precisely on this segment: workforce housing and Class B assets that compensate investors appropriately for risk.

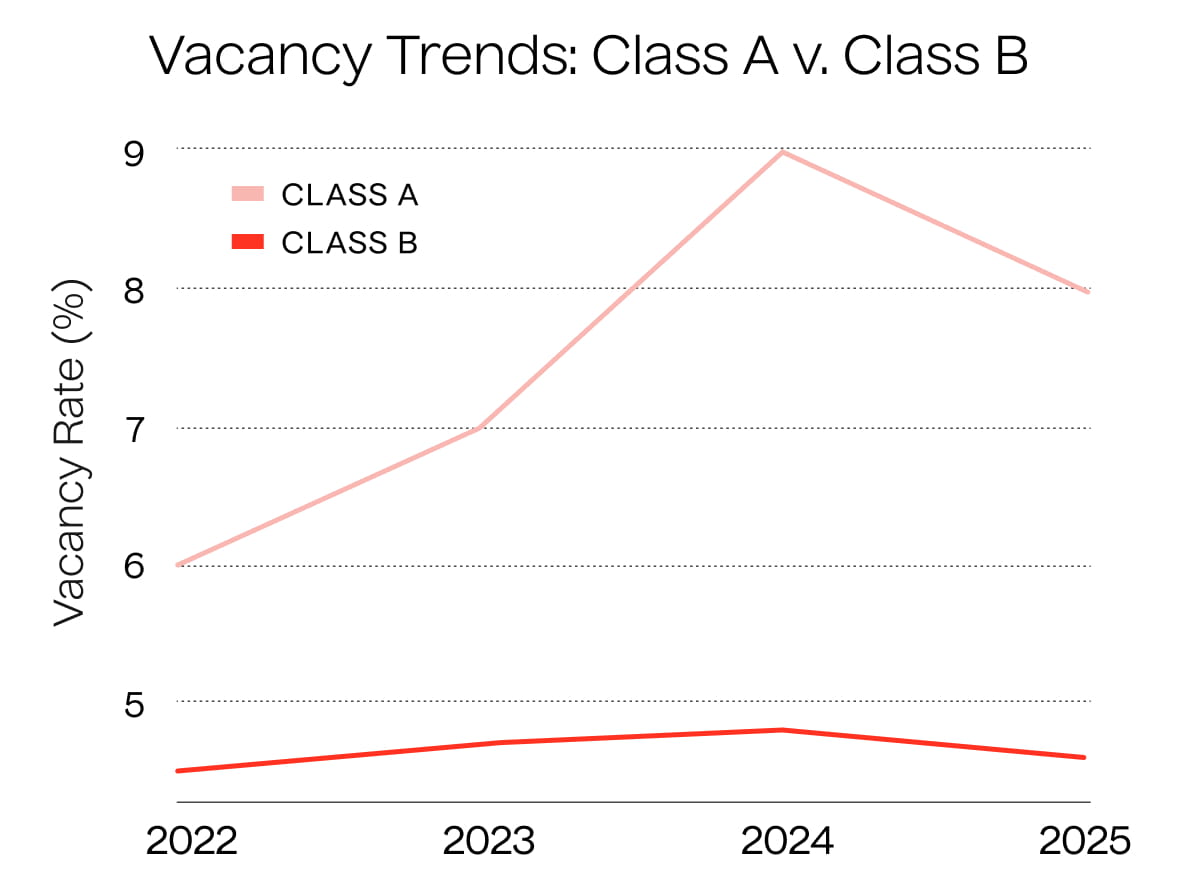

Market data supports this thesis. According to CBRE, U.S. multifamily vacancy rates declined by approximately 130 basis points from their early-2024 peak, reaching roughly 4.6% by Q3 2025, despite record new supply deliveries (CBRE U.S. Multifamily Market Outlook). This resilience has been most pronounced in Class B properties, where occupancy continues to outperform Class A across many markets.

Understanding Multifamily Real Estate Classes: Class A vs. Class B vs. Class C

Class A Multifamily: Prestige at a Price

Characteristics: New construction, premium urban or high-growth suburban locations, luxury finishes and amenity-heavy designs.

Financial Profile: Commands the highest rents, but yields are often compressed due to elevated acquisition costs.

Current Market Reality: Multifamily supply delivered in 2024 and 2025 added to the ever-growing Class A segment. This surge has resulted in widespread concessions and softer effective rents. At times, this can make it difficult to ascertain the true market rent and you risk the floor being lower than projected. According to RealPage and Yardi Matrix, Class A concessions reached their highest levels since the Global Financial Crisis in several major metros, with many properties offering six to eight weeks of free rent to maintain occupancy. Specifically, this is most pronounced in the sunbelt MSAs where herd mentality drove cap rates down and increased shovels in the ground. These same markets are dealing with the tough reckoning of higher rates and heavier new supply crushing both valuations and rent growth. (RealPage Analytics; Yardi Matrix National Multifamily Report).

While headline vacancy rates in Class A have stabilized near 9% in some markets, this stability has come at the expense of net operating income, as concessions and incentives erode cash flow.

Class B Multifamily: Yield With Control

Characteristics: Suburban assets generally 10–40 years old, low density, strong amenity offerings, good affordability metrics, solid fundamentals and functional layouts.

Tenant Base: Middle-income households and long-term renters seeking affordability without sacrificing quality.

Investment Opportunity: Class B assets offer genuine value-add potential through unit renovations, operational efficiencies, and professionalized management.

Performance Advantage: In many regions, Class B and workforce housing occupancies remain in the mid-90% range, consistently outperforming Class A. This reflects durable demand from households earning roughly 80%–120% of area median income, a segment closely tied to essential employment rather than discretionary spending (Urban Land Institute Workforce Housing Research).

Class C Multifamily: Higher Risk, Higher Maintenance

Characteristics: Older assets, often 40+ years old and inferior amenities.

Risk Profile: While Class C properties may offer headline yield, they frequently require heavy capital expenditures and intensive management, difficult tenant base to collect on, increasing operational risk and volatility.

Why Class B Multifamily Real Estate Works in 2026 and Beyond

1. Affordability Is the Primary Demand Driver

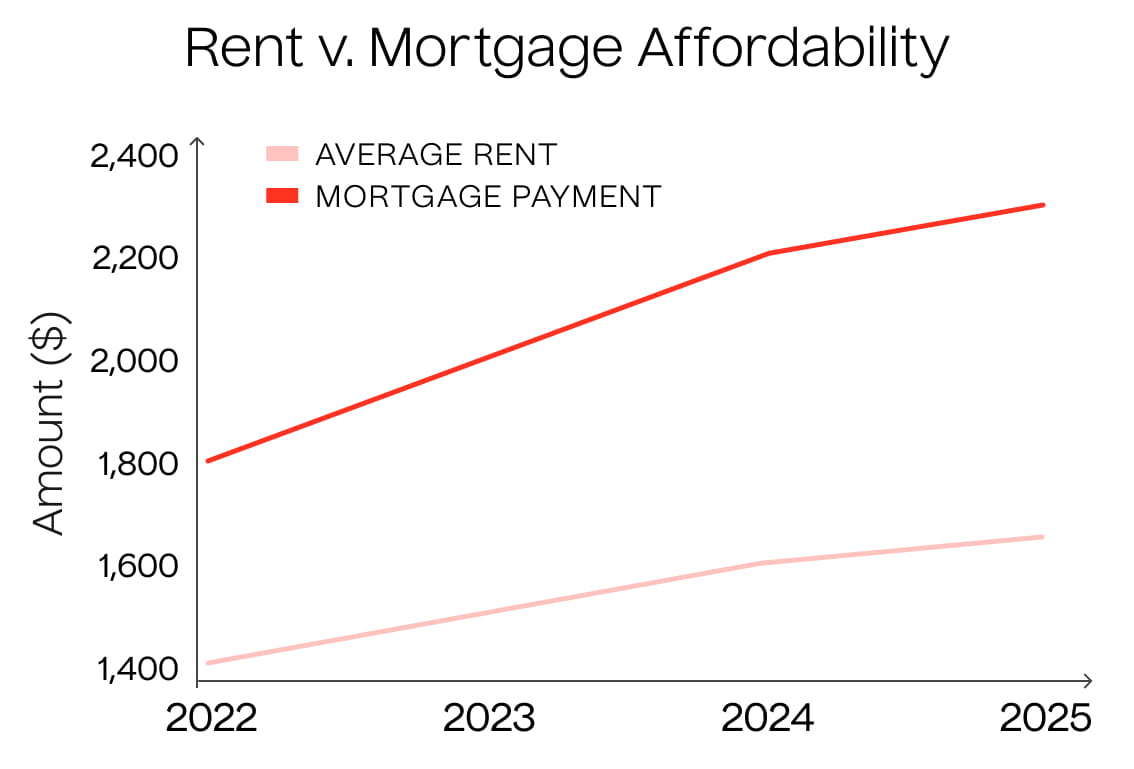

Affordability has become the defining factor in rental demand. Middle-income renters have increasingly been priced out of Class A, while the gap between renting and owning remains historically wide. According to Redfin and the National Association of Realtors, average monthly mortgage payments on newly originated loans are approximately 35% higher than average apartment rents, reinforcing the economic rationale for renting (Redfin Housing Affordability Index; NAR Housing Statistics).

Structural barriers to homeownership persist. The median age of first-time homebuyers reached 40 in 2024, the highest level on record, underscoring a long-term shift toward delayed or deferred ownership (NAR Profile of Home Buyers and Sellers).

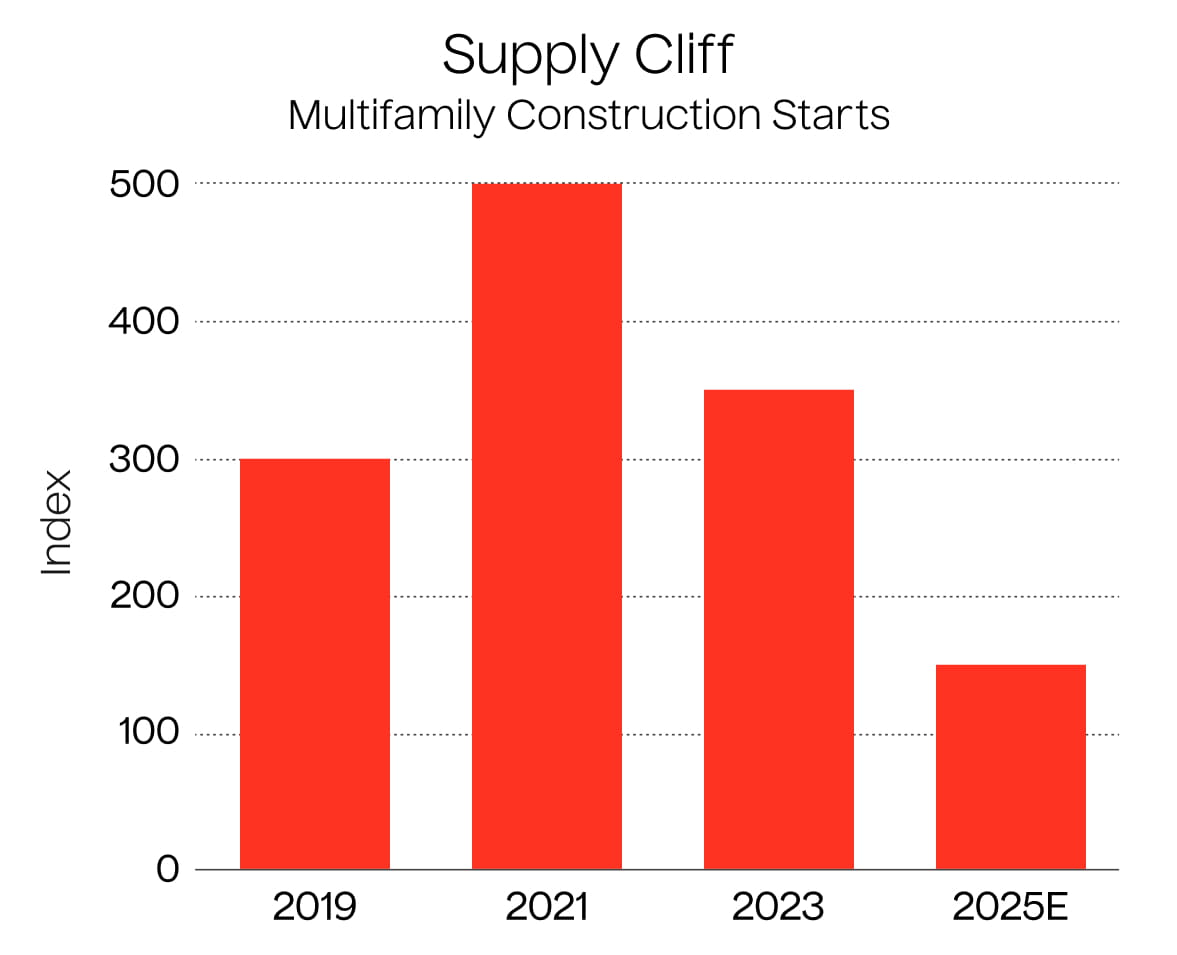

The Class B Supply Cliff

Developers continue to focus almost exclusively on luxury product due to construction costs, leaving virtually no new Class B supply in the pipeline. Dodge Construction Network data shows multifamily construction starts are down more than 70% from their 2021 peak, and the limited new starts that remain are overwhelmingly Class A (Dodge Construction Network Multifamily Outlook).

As 2024 deliveries taper off and new supply dries up in 2026, the scarcity of affordable, well-located Class B units is expected to drive occupancy and rent stability.

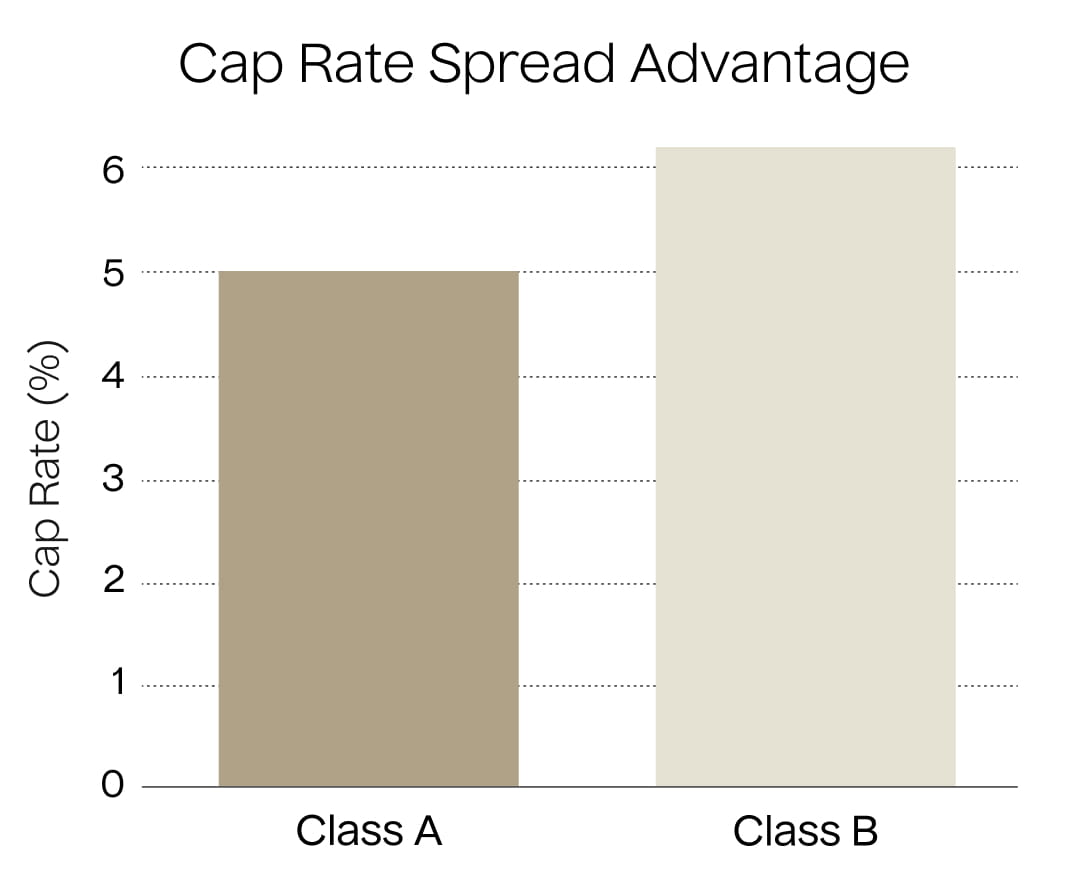

2. Wider Cap Rate Spreads and Stronger Day-One Cash Flow

Class B assets continue to offer materially wider yield spreads relative to Class A. According to CBRE and Green Street Advisors, Class B cap rates generally trade 50–150 basis points higher than comparable Class A assets, translating directly into stronger initial cash flow (CBRE Cap Rate Survey; Green Street Multifamily Outlook).

This yield buffer provides a margin of safety in a higher-for-longer interest rate environment and reduces reliance on market-driven appreciation.

3. Value-Add 2.0: Operational Upside Beyond Renovations

Modern value-add strategies extend beyond cosmetic upgrades. High-ROI improvements such as flooring, appliances, and lighting routinely generate good returns.

Equally important are operational enhancements. Technology-enabled living—smart thermostats, keyless entry, and managed Wi-Fi—has become a baseline expectation, particularly among Gen Z renters. Surveys from the National Multifamily Housing Council and Zillow show that a majority of Gen Z renters prioritize digital-first leasing, maintenance, and communication experiences (NMHC Renter Preferences Survey; Zillow Consumer Housing Trends).

Professional property management and systems such as utility billing (RUBS) further enhance net operating income without relying solely on rent increases.

4. Resilience Across Market Cycles

Class B multifamily has historically demonstrated all-weather performance. During downturns, Class A tenants often trade down into Class B to reduce housing costs, while in recoveries, Class C tenants trade up. This dual demand dynamic supports stable occupancy and income across cycles.

Workforce housing serves essential employees—healthcare workers, educators, logistics staff, municipal workers—whose employment is less sensitive to economic volatility. Freddie Mac and Fannie Mae research consistently shows workforce housing maintains occupancy even when rent growth slows (Freddie Mac Multifamily Research; Fannie Mae Multifamily Commentary).

5. Cash Flow First, Exit Second

Unlike trophy Class A investments that often rely on cap rate compression to meet return targets, Class B assets are underwritten for cash flow on day one. Fannie Mae research indicates that a significant portion of multifamily value appreciation over the past two decades was driven by pricing rather than NOI growth—a dynamic that has slowed materially since 2022 (Fannie Mae Multifamily Research).

In this environment, durable income matters more than speculative appreciation.

Market Trends Supporting Class B in 2026

Institutional capital continues to rotate toward multifamily, with workforce housing favored for its stability. PwC’s Emerging Trends in Real Estate report shows that over half of institutional investors rank multifamily as the top sector for long-term performance (PwC Emerging Trends in Real Estate).

At the same time, the Federal Housing Finance Agency increased the 2026 multifamily loan purchase caps for Fannie Mae and Freddie Mac to $88 billion each, improving liquidity for well-located workforce housing assets (FHFA Announcement).

Conclusion: Why Class B Multifamily Wins in 2026

If Class A is defined by prestige and Class C by risk, Class B is defined by balance.

In 2026, that balance is precisely what disciplined investors should target. Class B multifamily offers durable tenant demand, superior risk-adjusted yields, and controllable upside through operations rather than speculation.

Greg Fink

Greg Fink is the Chief Investment Officer of Lightstone DIRECT and the Vice President of Acquisitions at Lightstone. Under Lightstone DIRECT, Greg manages day-to-day operations, provides strategic oversight for all investments, and leads DIRECT’s long-term growth trajectory.

At Lightstone, Greg is also the Vice President of Acquisitions, where he leads Lightstone’s multifamily investments nationwide. He joined Lightstone in 2015 and has closed over $3.0BN worth of multifamily acquisitions and dispositions across 16,000 units nationwide. He oversees all aspects of a transaction from strategy, sourcing, structuring, financing, and closing. Mr. Fink graduated from New York University with a B.S. in Communications and a M.S. in Real Estate Finance.