Learn more about everything Lightstone DIRECT has to offer

Generating magic link...

Understanding 1031 Exchanges: A Guide for Accredited Real Estate Investors

Understanding 1031 Exchanges

A Guide for Accredited Real Estate Investors

Tax Deferral Strategies, Investment Vehicles, and Comparative Analysis

What Is a 1031 Exchange?

A 1031 exchange, named after Section 1031 of the Internal Revenue Code, is one of the most powerful tax-deferral tools available to real estate investors. In its simplest form, a 1031 exchange allows an investor to sell an investment property and reinvest the proceeds into a new like-kind property while deferring the capital gains taxes that would otherwise be owed on the sale. This mechanism has been a cornerstone of U.S. real estate investment strategy for decades, enabling investors to preserve and compound their wealth over time.

The concept is straightforward: instead of paying federal and state capital gains taxes, depreciation recapture taxes, and the Net Investment Income Tax (NIIT) at the time of sale, the investor rolls the full proceeds into a replacement property. The tax liability is not eliminated but rather deferred until the replacement property is eventually sold outside of a 1031 exchange. In practice, many investors execute serial 1031 exchanges throughout their lifetimes, and upon death, their heirs may receive a stepped-up cost basis, effectively eliminating the deferred tax liability altogether.

To qualify, both the relinquished property (the one being sold) and the replacement property must be held for investment or productive use in a trade or business. Personal residences and properties held primarily for resale (such as fix-and-flip projects) do not qualify. The replacement property must be of like-kind, which in the context of real estate is broadly defined. An investor can exchange an apartment building for a retail center, an industrial warehouse for raw land, or virtually any combination of real property types.

Critical Timing Requirements

1031 exchange investors must adhere to the strict timing requirements established by the IRS. There are two critical deadlines that every investor must understand, and failure to meet either one will disqualify the exchange entirely, resulting in an immediate tax liability.

The 45-Day Identification Period

Beginning on the day the relinquished property closes, the investor has exactly 45 calendar days to formally identify potential replacement properties. This identification must be made in writing and delivered to a qualified intermediary or other designated party. The investor may identify up to three properties of any value (the Three-Property Rule), or any number of properties whose combined fair market value does not exceed 200% of the relinquished property’s sale price (the 200% Rule). There is also a 95% Rule that allows identification of any number of properties provided the investor ultimately acquires at least 95% of the aggregate identified value.

The 180-Day Exchange Period

The investor must close on one or more of the identified replacement properties within 180 calendar days of the sale of the relinquished property. This deadline is absolute and cannot be extended, even if it falls on a weekend or holiday. It is worth noting that the 180-day period runs concurrently with the 45-day identification window, not sequentially. In other words, the total time from closing on the sale to closing on the purchase is 180 days, not 225 days.

The Role of the Qualified Intermediary

A qualified intermediary (QI) is an essential participant in every 1031 exchange. The QI holds the sale proceeds in escrow during the exchange period, ensuring the investor never takes constructive receipt of the funds. If the investor touches the money at any point, the exchange is disqualified. The QI facilitates the transfer of funds from the sale closing directly to the replacement property closing, maintaining the integrity of the exchange throughout the process.

Hypothetical Comparison: Taxable Sale vs. 1031 Exchange

To illustrate the tangible financial impact of a 1031 exchange, consider the following hypothetical scenario comparing two investors who each sell an identical investment property. One pays the taxes and reinvests in the stock market, while the other executes a 1031 exchange and reinvests passively in an individual real estate deal.

Scenario Setup

Both investors sell a property for $1,000,000 with an original cost basis of $400,000 and accumulated depreciation of $200,000. The resulting capital gain is $600,000. The tax implications for the investor who does not execute a 1031 exchange are as follows: federal capital gains tax at 20% ($120,000), state income tax at 5% ($30,000), Net Investment Income Tax at 3.8% ($22,800), and depreciation recapture at 25% on $200,000 ($50,000), resulting in a total tax liability of $222,800.

Key Assumptions

Year-by-Year Growth Comparison

Growth Comparison: Taxable Sale vs. 1031 Exchange

Analysis of Results

Scenario A: Taxable Sale + S&P 500. After paying $222,800 in taxes, the investor has $777,200 to invest in an S&P 500 index fund. Assuming a 10% annualized return, this grows to approximately $1,251,688 after five years, representing a gain of $474,488 on the invested capital.

Scenario B: 1031 Exchange + Passive Real Estate Deal. The investor defers all taxes and reinvests the full $1,000,000 into a passive real estate deal. After a 6% upfront fee load, the net invested capital is $940,000. Assuming a 10% annualized return (inclusive of a 6% annual distribution yield), the investment grows to approximately $1,513,879 after five years, representing a gain of $573,879 on the originally deployed capital.

The difference between the two outcomes is approximately $262,191, or a 21% advantage in favor of the 1031 exchange. This gap is driven by two compounding factors: the investor preserved $222,800 in tax savings that remained invested from day one, and the real estate deal achieved a higher annualized return than the stock market index.

Conclusion: Which Path Is Better for the Investor?

Based on the assumptions in this analysis, the 1031 exchange into a passive real estate deal is the clear winner from a total wealth accumulation perspective. The investor ends the five-year period with approximately $1,513,879 compared to $1,251,688, a difference of nearly $262,191. When comparing these two scenarios, the most important takeaway is that the advantage of the 1031 exchange does not rely on assuming higher investment returns. In this analysis, both the S&P 500 investment and the real estate investment are assumed to generate the same 10% annualized return, allowing us to isolate the impact of tax deferral alone.

Investment Approaches for a 1031 Exchange

Once an investor decides to execute a 1031 exchange, the next critical decision is how to deploy the capital into a replacement property. There are three primary approaches, each offering a distinct blend of control, passivity, and risk. Understanding the tradeoffs between these options is essential for making an informed decision that aligns with the investor’s financial goals and lifestyle preferences.

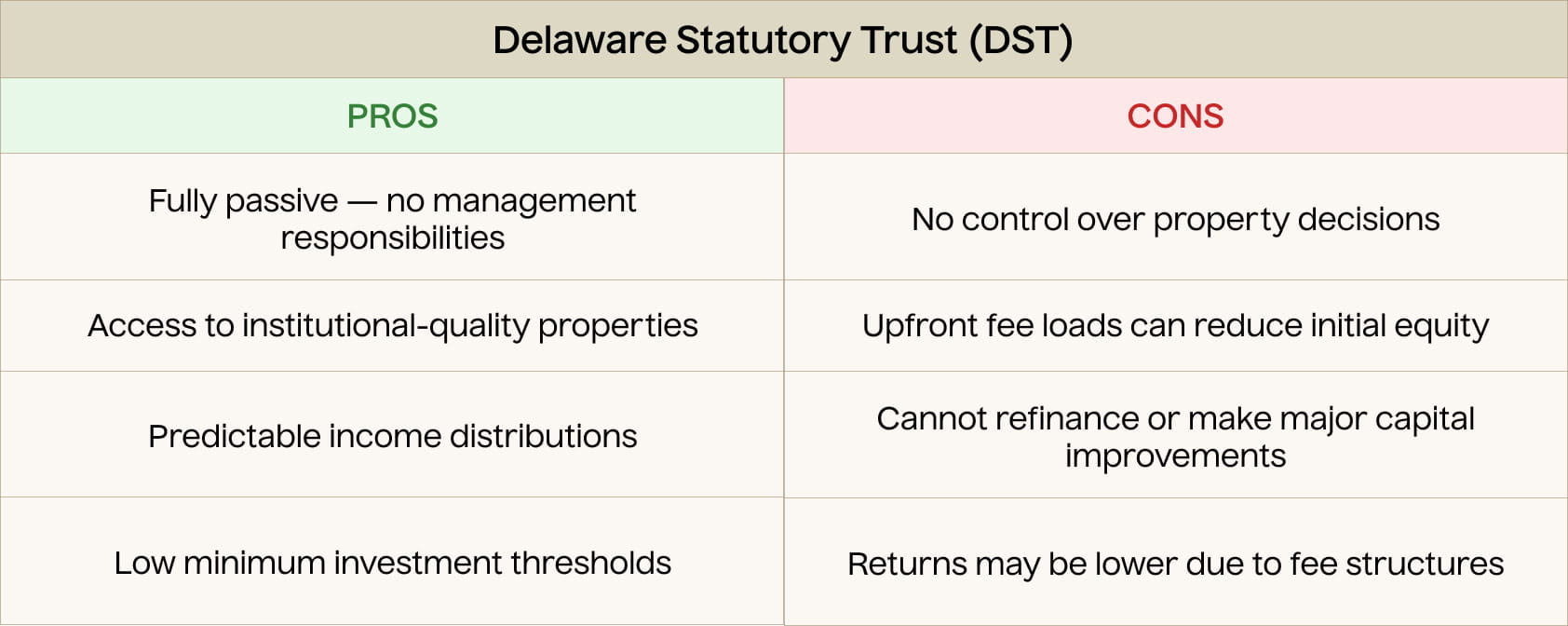

Option 1: Delaware Statutory Trust (DST)

A Delaware Statutory Trust is a legal entity that holds title to one or more investment properties, allowing multiple investors to own fractional, beneficial interests in institutional-quality real estate. DSTs are specifically structured to qualify as like-kind replacement property under Section 1031, making them an ideal solution for investors seeking a fully passive investment. The sponsor of a DST handles all property management, leasing, financing, and eventual disposition, while investors receive their pro-rata share of cash distributions and any appreciation upon sale.

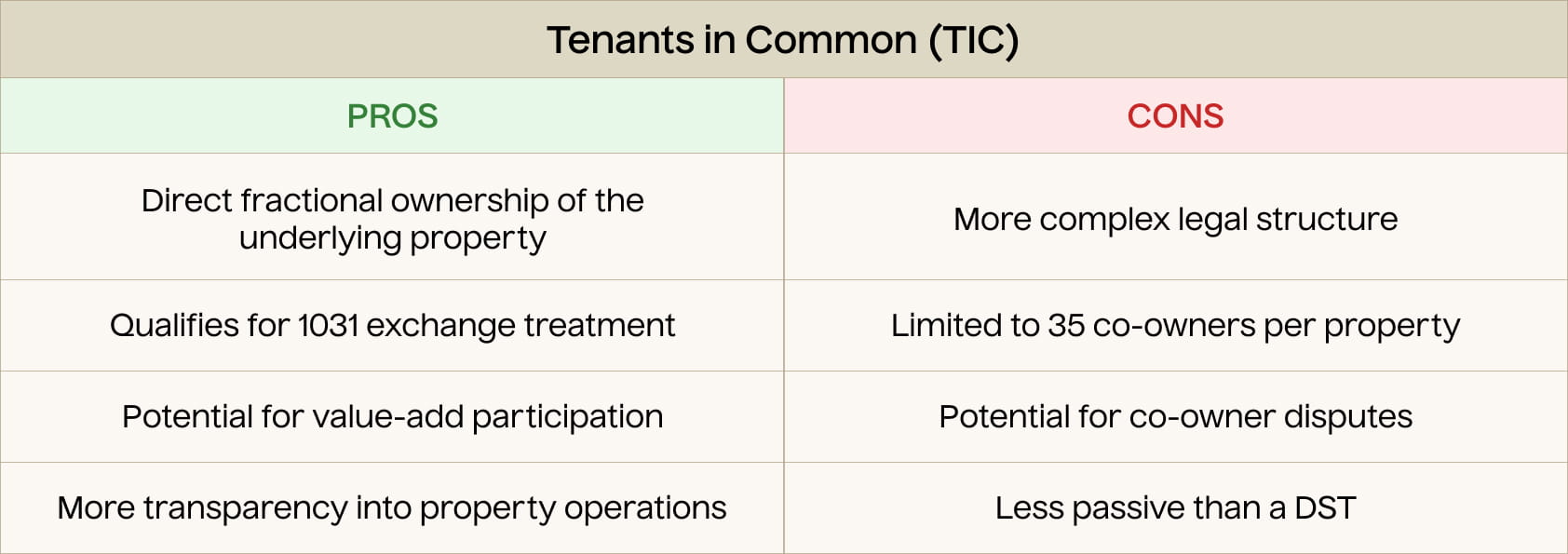

Option 2: Tenants in Common (TIC)

A Tenants in Common structure allows multiple investors to hold direct, undivided fractional ownership interests in a single property. Unlike a DST, TIC investors hold actual title to their portion of the real estate, providing a degree of transparency and control that some investors prefer.

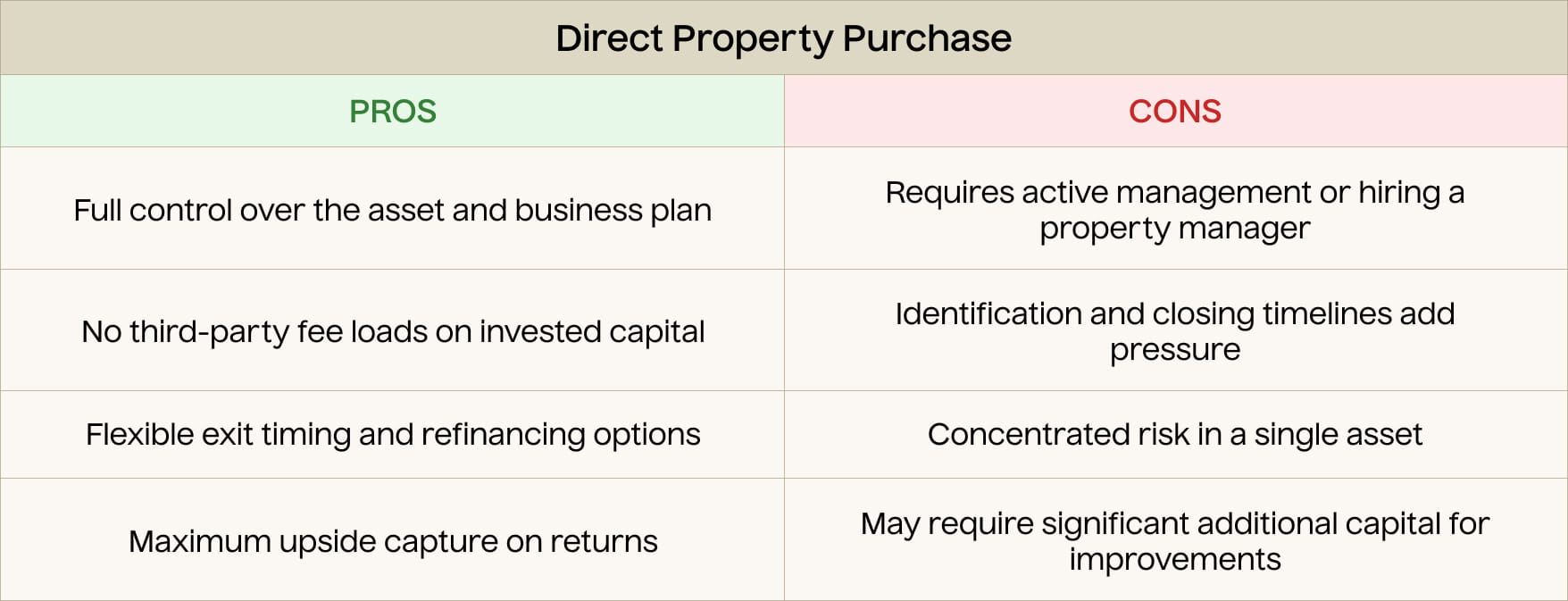

Option 3: Direct Property Purchase

The most traditional approach to a 1031 exchange is the direct acquisition of a replacement property. This gives the investor full ownership, control, and decision-making authority over the asset. Direct purchases offer the greatest potential upside, as the investor captures 100% of the appreciation and income without sharing returns with other co-investors or paying sponsor fees. However, this approach also requires the most active involvement and carries concentrated risk in a single asset.

Why Many DSTs Have Limitations That Matter for Value-Add Strategies

A DST is generally structured to maintain a “trust” posture. In practical terms, that means the structure often avoids the kind of active, discretionary behavior that might make it resemble an operating business. To stay in that lane, DSTs are commonly associated with constraints on things like:

- Renegotiating or materially changing leases

- Raising new equity or doing capital calls

- Refinancing or renegotiating debt terms in a discretionary way

- Executing major redevelopment or significant property modifications

- Buying additional properties or fundamentally changing the asset mix

Even when there are limited exceptions, the overall posture is intentionally conservative. For many investors, that’s a benefit. If you want a stable hold where the plan is essentially to collect contractual rent and distribute it, a DST can be a clean solution.

But those limitations can become a drawback if the investment thesis depends on active execution—especially strategies that require multiple levers like renovations, operational improvement, ancillary income programs, or a dynamic approach to leasing and capital planning.

In other words, DSTs tend to shine when the plan is “hold a stable asset with limited change.” They are often less natural for strategies where “improvement” is the primary driver of return.

The Investor Goal Many People Share: Cash Flow Plus Upside

Many exchangers are trying to solve for two goals at the same time:

- Preserve tax deferral through a qualifying 1031 replacement investment

- Maintain attractive returns, which often includes both ongoing cash flow and a path to equity upside

In the DST marketplace, the easiest way to deliver predictable income is often through highly stabilized assets—sometimes at pricing that reflects that stability. The result can be a return profile that is steady but potentially less driven by operational value creation.

Investors who still want to participate in upside—especially upside driven by execution—often look for structures that allow for a more active business plan while still pursuing 1031 eligibility. That is where TICs can be compelling.

Why a TIC Can Be Better Positioned for Value-Add Execution

A TIC structure is built around the idea that investors are direct co-owners of the real estate. When properly structured, a TIC can allow:

- Professional, sponsor-led day-to-day management

- A business plan that includes operational improvements and measured renovations

- Governance terms that preserve the “co-ownership” character needed for 1031 purposes, while still being workable in practice

The key advantage is not that TICs magically create returns. The advantage is that, structurally, TICs can often accommodate a broader set of real-world ownership and operating activities than a typical DST.

That flexibility matters most when the sponsor’s underwriting is tied to actions like:

- Stabilizing occupancy and improving tenant retention

- Executing targeted renovations to drive rent premiums

- Adding or optimizing ancillary income (for example, utilities, internet, parking, pet programs, insurance programs)

- Creating efficiencies through scale and professional management

- Making disciplined capital decisions based on market conditions

A measured value-add plan is still a risk-managed plan. It isn’t about “swinging for the fences.” It’s about creating multiple paths to improving net operating income and strengthening the asset’s long-term position. Unlike Delaware Statutory Trusts (DSTs), TICs allow active management, refinancing, property improvements, and lease flexibility.

In short, the TIC structure is more extensible to Lightstone’s typical light value-add strategy, which is why Lightstone DIRECT makes use of a TIC structure in offering 1031 exchange multifamily investments. In our manager-led model, Lightstone handles day-to-day operations, while certain major decisions are subject to defined approval thresholds. This is an important practical detail. A value-add plan requires a manager who can operate decisively—leasing, renovations, vendor management, and program execution cannot be run by committee. At the same time, the governance is designed to preserve the co-ownership character associated with TIC structures intended for 1031 use.

Conclusion: Why and How a 1031 Exchange May Fit Your Portfolio

For investors with a long-term horizon, a tolerance for illiquidity, and a desire to maximize total wealth while generating meaningful current income, the 1031 exchange into a quality real estate investment represents a compelling strategy. The combination of tax deferral, income generation, and the potential for appreciation creates a powerful wealth-building framework that is difficult to replicate in the public markets.

Whether a DST, TIC, or other structure is the best fit for your 1031 Exchange investing depends on how active you plan to be in management of the investment, and what your return objectives are (on top of tax deferral). If you seek a blend of tax-deferred strategy and upside, Lightstone DIRECT’s TIC-structure, light value-add multifamily strategy may be worth a close look.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment, tax, or legal advice. Past performance is not indicative of future results. All assumptions and projections are hypothetical and may not reflect actual market conditions. Investors should consult with their qualified tax advisor, attorney, and financial professional before making any investment decisions or engaging in a 1031 exchange.