Learn more about everything Lightstone DIRECT has to offer

Generating magic link...

The Lightstone Letter

Welcome to The Lightstone Letter, a biweekly newsletter from the investment team at Lightstone DIRECT. In each edition of The Lightstone Letter, we share exclusive content, real estate investing education, market perspectives, and new angles on our live investment opportunities.

You can also follow the newsletter (and other Lightstone DIRECT activity) on our LinkedIn page.

Edition 2

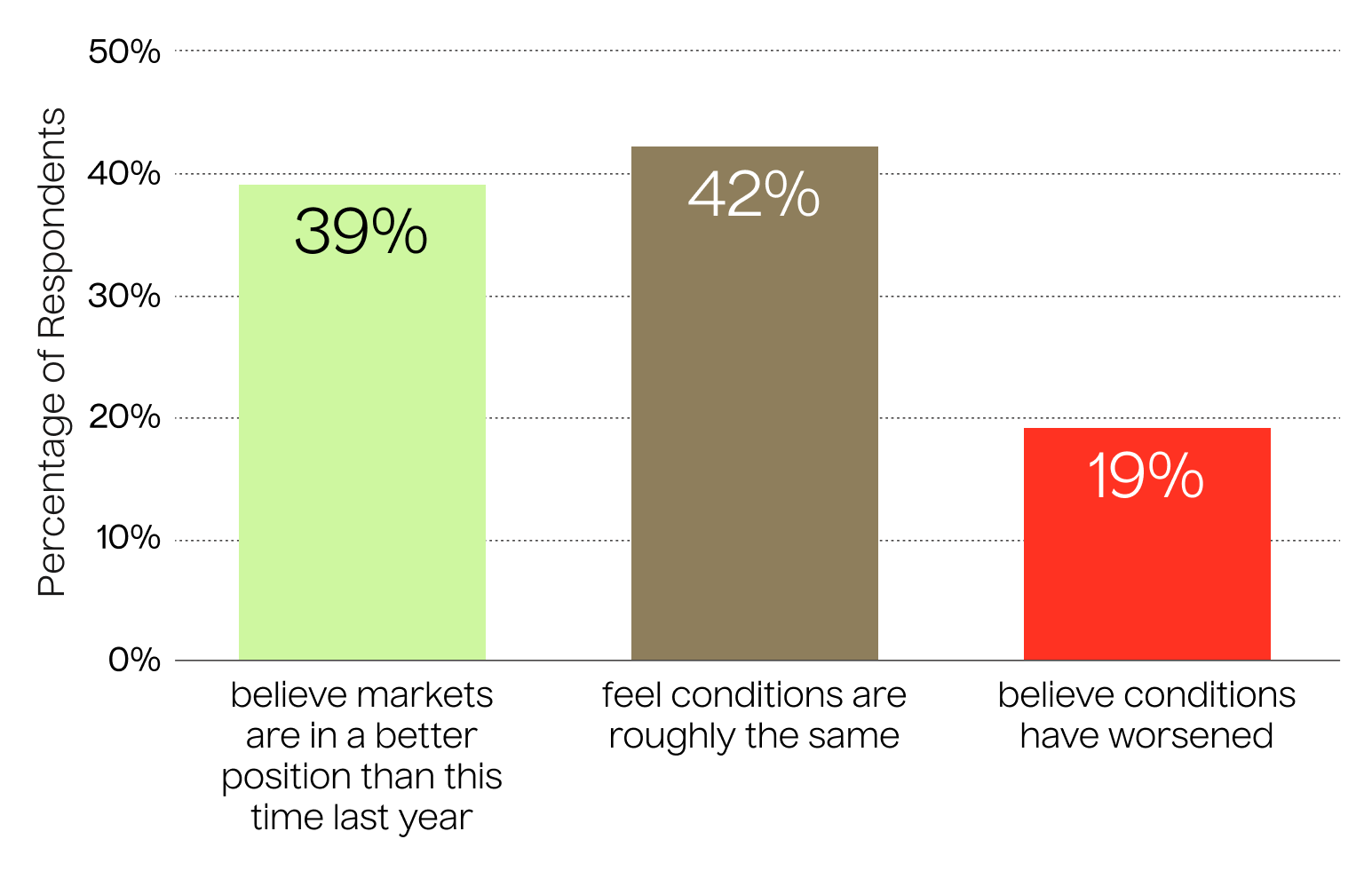

Last month, we surveyed the Lightstone DIRECT investor community to understand how individual LPs are thinking about real estate as we entered 2026.

The responses offered a clear picture: investors are interested but cautious, favoring current yield over appreciation, downside protection over growth, and proven managers over first-time sponsors.

This pattern also showed up after the GFC. In PwC/ULI’s Emerging Trends in Real Estate 2011, respondents described a market with “hopeful signs” of improvement, but emphasized lower return expectations and a preference for well-located assets with strong cash flow. In other words, when recovery begins, investors usually aren’t piling into more speculative investments. They gravitate toward current income and asset quality.

Our survey results suggest individual investors are approaching this environment in much of the same way and this behavior feels consistent with the start of a new cycle.

A Note on the Headlines

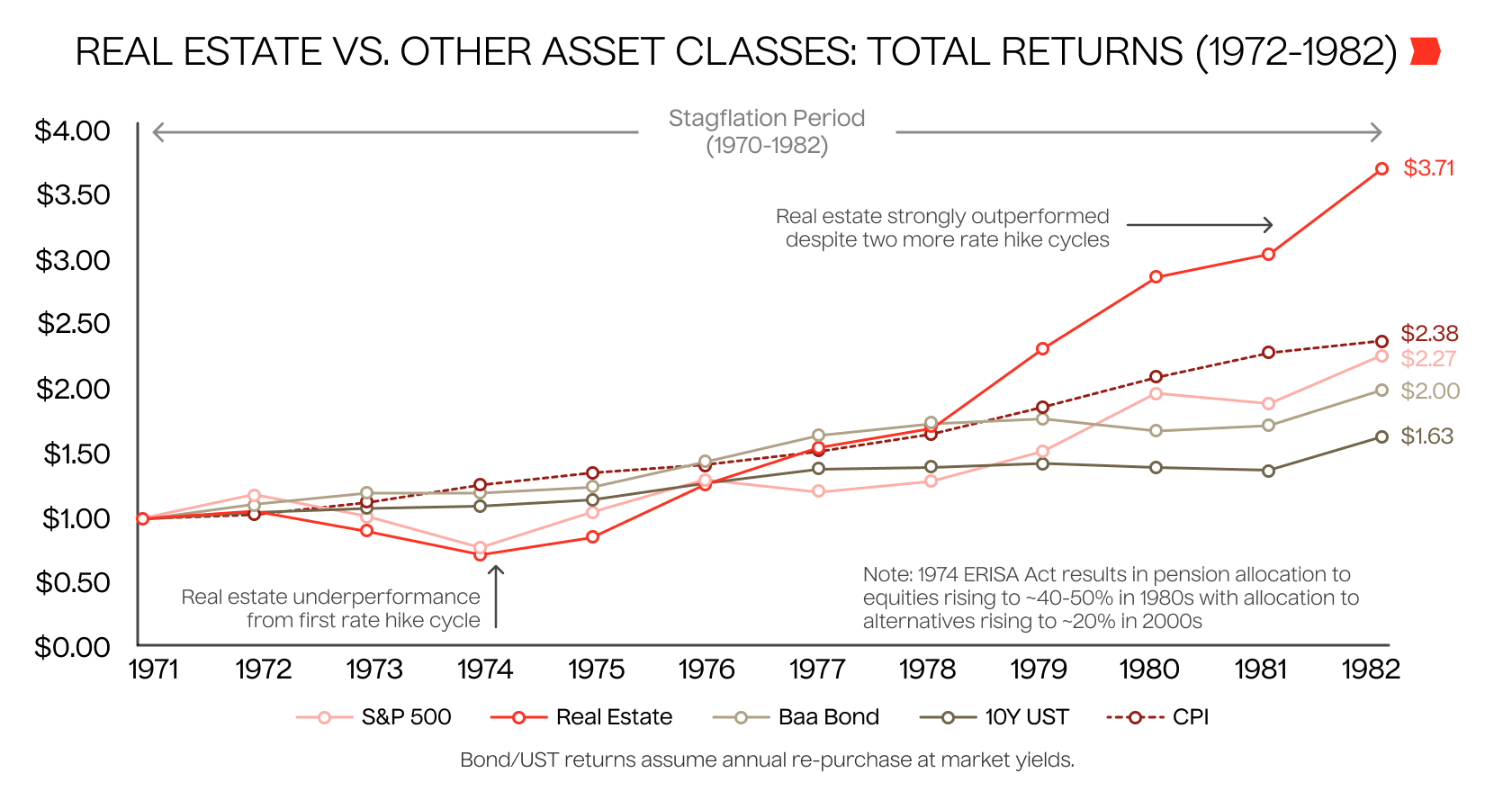

We would be remiss in not mentioning what’s happened since we surveyed our investor community. Conflict in the Middle East has driven what the International Energy Agency describes as “the biggest energy shock in history.” While we can’t predict how this episode of geopolitical tension plays out, history does offer a blueprint as the potential relative performance of asset classes. Notably, during the OPEC crisis of the 1970s — the largest prior energy shock on record — real estate outperformed the S&P by a wide margin on a real and inflation-adjusted basis. The conditions then mirror the conditions now, and a go-forward case for private real estate as a potentially defensive asset class: elevated interest rates and construction costs may act to further restrict supply; consumers may tamp down on discretionary spending, potentially impacting public equities, while demand for essential housing and logistics remains stable.

Again, we cannot forecast the long-term impact of the current crisis, and our fundamental viewpoint is unchanged: a real estate recovery is now underway. That said, prior energy shocks and stagflationary periods do point to private real estate as a potential safe haven for defensive-minded investors.

What to Look for in a Market Recovery

One of the biggest concerns we hear about from investors is whether they are stepping back into the market too early. It’s a fair question because unlike public equity markets, private markets move slowly, and it took 2 to 3 years for the real estate market to fully reprice to a higher interest rate environment. That kind of prolonged repricing typically changes investor behavior in important ways. The first-order effect of a prolonged downturn is usually caution. And that caution can linger even after prices have mostly reset.

At Lightstone, we’ve seen a steady increase in capital markets activity, with several indicators pointing to improving momentum. Property valuations and transaction volume tend to move together over time, and since the market troughed in early 2024, transaction volumes have risen by almost 50% with consistent gains over nearly two years.

While transaction volume is still well below the Q2 2022 peak, this steady recovery is important. In our view, it suggests the market is moving through the early stages of normalization rather than continuing to search for a bottom. The takeaway here is that the worst of the repricing appears to be behind us, and capital is slowly returning to the market.

Broader investor sentiment points in the same direction. According to CBRE’s 2026 North America Investor Intentions Survey, 74% of commercial real estate investors expect to increase acquisitions this year, reflecting growing confidence that pricing has reset and fundamentals are stabilizing. Our investor survey shows a similar pattern among individual LPs with 65% of respondents planning to allocate more capital to private market real estate, compared with just 14% who expect to reduce exposure. Together, these results suggest that confidence is improving, even if investors remain selective about where and how they put capital to work.

Cautious Optimism

While we believe the worst of the repricing is likely behind us, most investors are not approaching today’s market with unchecked enthusiasm. Instead, sentiment appears constructive, which is often what an early-cycle recovery looks like.

Our survey results point in that direction. Most respondents see stabilization taking hold across real estate markets, but few are ready to call for a full recovery. Expectations remain grounded, and that view aligns with our thinking in that this recovery is likely to be gradual and uneven, shaped by sector-specific supply dynamics, local demand conditions, and the pace at which capital re-engages.

The investors we hear from today are focused on cash flow, realistic underwriting, and whether the sponsor's interests are genuinely aligned with theirs.

One respondent put it plainly:

“I’m increasingly focused on risk-adjusted yield, not projected IRR. Anyone can model a 17% IRR; very few can deliver it without aggressive rent-growth assumptions, optimistic exit caps, or leverage that only works in perfect conditions. Manager alignment and transparency matter more than ever.”

Another investor highlighted the role private real estate plays within a broader portfolio:

“[Private-market real estate] provides good non-correlated returns and tax benefits but sponsor reliability and due diligence is crucial.”

A third distilled it to six words:

“Buyers need to be very selective.”

These responses reflect that a premium on execution and alignment has risen, while the tolerance for speculative assumptions has fallen. Sponsors who can demonstrate both operational advantages and conservative underwriting are the ones attracting capital.

In multifamily, strong renter demand and a thinning development pipeline are beginning to create a more favorable backdrop. But just as notable as the improving setup is how investors are responding to it. The qualitative survey responses suggest a clear emphasis on durability, discipline, and alignment.

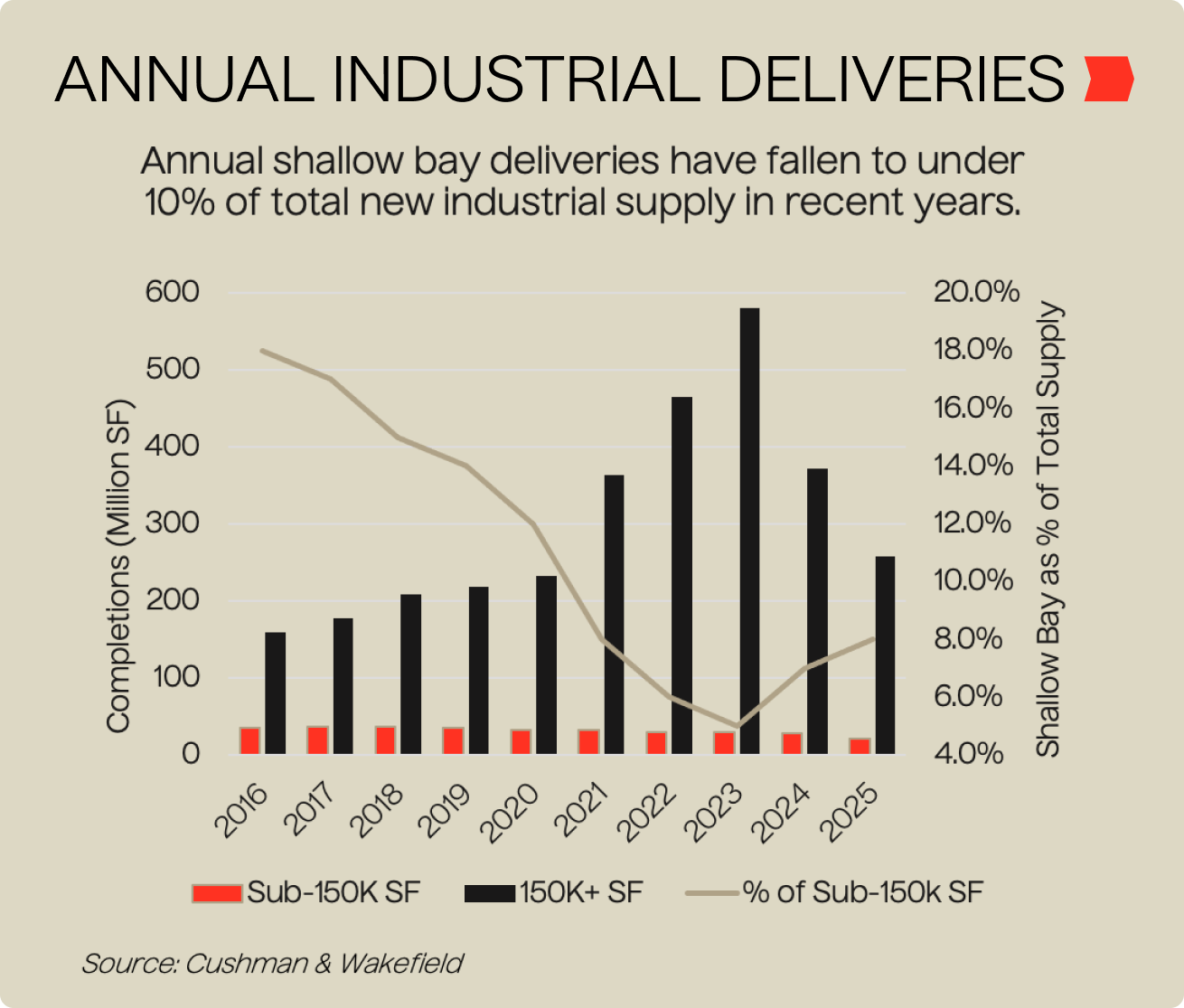

While supply pipelines are thinning across most CRE asset classes, the trends are not uniform. Fundamentals are not necessarily improving across all CRE sectors at the same rate, on the same timeline. While new supply is falling for shallow bay industrial, supply of this sub-asset class has lagged behind other types of industrial real estate for many years.

The Asset Classes Investors Favor

When asked which property sectors appear most attractive entering 2026, two asset classes stood out clearly among respondents:

Industrial and multifamily.

Again, this aligns closely with broader industry research.

Despite short-term volatility, the long-term outlook for both sectors remains supported by structural demand drivers:

- Housing affordability challenges continue to support renter demand, particularly in workforce housing segments. New apartment completions are expected to decline by over 30% over the next 12 months. Shorter supply, more expensive inputs, and tighter capital conditions all favor light value-add strategies, where in-place occupancy is strong and there is a clear path to NOI growth with modest cap ex.

- E-commerce, reshoring, and supply chain restructuring continue to support logistics and light industrial space. We see shallow bay industrial as offering compelling relative value over larger facilities.

Even with recent supply surges, fundamentals remain durable. For example, national forecasts expect multifamily occupancy to improve as the current delivery wave subsides and demand absorbs new units over the next several years.

We believe the repricing that has occurred over the past several years has created an environment where quality assets can increasingly be acquired at prices that reflect realistic assumptions rather than peak-cycle optimism.

At the same time, supply pipelines across key sectors are beginning to thin, setting the stage for improving fundamentals in the years ahead, at least within certain sectors and markets.

In our view, the opportunity set in this environment favors individual investors who:

- Focus on durable cash flow rather than speculative growth

- Partner with experienced operators

- Prioritize alignment of incentives

That perspective appears to be shared by a growing number of investors within the Lightstone DIRECT community. The collective mindset entering this new phase of the cycle is exactly the one required to navigate it successfully.

Edition 1

The past several years have marked one of the most challenging periods for real estate investors in over a decade. Property valuations have slowly adjusted to a higher interest rate environment, and markets have worked through a surge of new multifamily and industrial supply stemming from the COVID-era development cycle.

Yet despite these headwinds, property level fundamentals have been resilient, and we’ve seen this firsthand across our $12B portfolio at Lightstone. As an example, we executed 21 new leases in 2025 on over 1.1 million square feet of industrial space, and 19 out 21 of those leases were executed at lease rates above pro-forma with no rent concessions. Within our multifamily portfolio, rents grew 3.0% year-over-year, while net operating income increased 4.7%, exceeding our internal targets for the year.

This combination of portfolio-level performance and broader market data gives us conviction that we are in the early stages of a real estate recovery. Several indicators support this view:

Property Pricing Has Reset

The Green Street Commercial Property Pricing Index (CPPI) shows that following valuation declines of approximately 20% in industrial and 35% in multifamily from 2022 through 2024, pricing has found a floor and begun to stabilize over the past 12 months. Additionally, industrial and multifamily transaction volumes have rebounded meaningfully, up 35% and 60%, respectively, since the Q1 2023 trough, suggesting that buyers and sellers are increasingly aligned on price and activity is beginning to normalize.

Supply May Continue to Fall

Record supply levels in 2023 and 2024 created occupancy challenges across the Class A multifamily and industrial sectors, resulting in flat to negative rent growth across many markets.

However, higher interest rates and tighter financing conditions have brought new development activity to a standstill, with annual deliveries projected to decline over 65% by 2027. Over the next few years, we believe this limited supply pipeline will support rent growth and create a stronger foundation for robust cash flow and long-term capital appreciation.

Capital Market Liquidity is Returning

In addition to higher interest rates and elevated supply, regional banks largely pulled back from commercial real estate lending over the past several years, further constraining transaction activity and limiting price discovery.

At Lightstone, however, we are seeing renewed engagement from multiple lenders and transactions beginning to clear at more rational pricing levels.

No cycle perfectly echoes the past. That said, our 40 years of experience tells us that periods like this tend to reward real estate operators who can exercise patience and be disciplined on price. From our perspective, we’re entering a period where not every sector or market will perform the same, and selectivity will matter more than it did in the previous cycle.

We will continue to focus on acquiring assets at an attractive discount to replacement cost with strong going-in yields. We seek to drive returns through light value-add strategies, focused on targeted capital improvements, and mark-to-market leasing strategies. Our approach prioritizes durable cash flow and downside protection, with multiple paths to value creation.

Our 2026 Market Outlook will substantiate this thesis using first-party observations from Lightstone’s portfolio and operating platform.

Soren Godbersen

Soren Godbersen is Chief Growth Officer at Lightstone DIRECT, where he oversees investor experience, day-to-day operations, marketing, and strategic direction of the group. Previously Godbersen was Chief Growth Officer at EquityMultiple, a category-defining real estate investment platform for accredited investors where he led the Marketing and Investor Relations Teams, helping to grow the firm’s AUM to nearly $1B, and investor network to over 5,000 individual high-net-worth investors. Godbersen holds a Bachelor's of Arts in Economics with Honors from Whitman College.