An Investor’s Guide: Industrial Real Estate Sub-Asset Types

Introduction: The Fundamentals of Industrial

Industrial real estate presents one of the most dynamic and compelling investment opportunities. Secular trends such as e-commerce adoption, supply-chain reshoring, and the rising need for logistics efficiency continue to reshape how goods move across the country. As a result, industrial assets can offer stable cash flows, resilient demand, and long-term growth potential.

But industrial isn’t one-size-fits-all. The sector includes very different property types, each with its own building characteristics, tenant base, and risk/return profile. For individual investors more familiar with multifamily, understanding these differences is essential. Cash flow stability, rollover risk, credit quality, and management intensity can vary meaningfully from one industrial subtype to the next.

In this guide, we’ll think like an owner should and break down the major subtypes, explain what makes them attractive to investors, and share examples from Lightstone’s portfolio where possible.

Nuts and Bolts: Understanding the Unique Ingredients

Just like evaluating ingredients in a cookbook, industrial developers and investors must evaluate the different aspects that make up each type of industrial property. The “nuts and bolts” are specifications and locational factors that determine how tenants use space, and how investors capture value. These are the baseline terms every investor should understand:

Building Specifications

- Bay Depth – TheDistance from loading docks to the back wall. Shorter bays suits smaller tenants and multi-tenants layouts, while deeper bays are designed for larger distributors with high throughput needs.

- Ceiling / Clear Height – The usable vertical space for racking and automation. Lower heights are efficient for local service businesses, but modern logistics and e-commerce tenants will need 32-40 feet of clear height to maximize cubic capacity.

- Dock Doors – The main entry and exit for goods movement. The number, spacing, and design of dock doors directly impact efficiency, again, where this scales with tenant need.

- Power Capacity – The available electrical load of the building. Standard warehouses need modest power, but cold storage, manufacturing, and automation-heavy operations require significant capacity or the ability to upgrade.

Locational Factors

- Proximity to Consumers – Being five miles closer to a metro core can mean hours saved per day in deliveries, which translates into sticky tenants willing to pay premium rents.

- Access to Transportation – Many big box tenants rely on heavy use of highways, ports, rails, and airports to move goods regionally and nationally.

- Labor Pool Availability – A well located property without great proximity to labor forces could struggle to keep tenants if turnover or shortages increase. Investors should consider not only where the building sits, but where its employees live.

- Zoning and Land Constraints – Scarcity drives value. Infill and shallow bay assets can command premium rents with limited supply competition, while suburban bulk sites are easier to replace.

The Breakdown of Asset Types

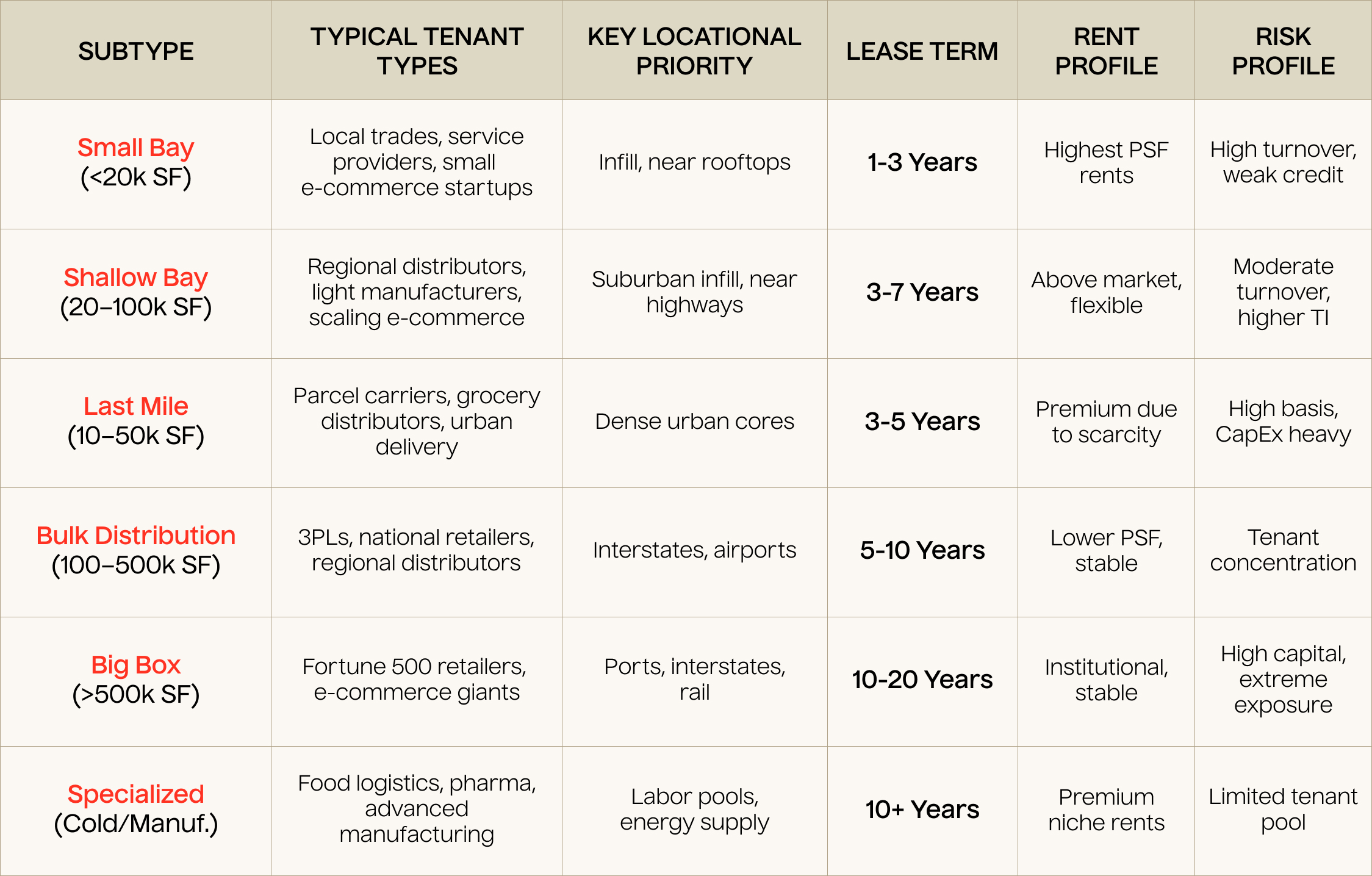

Small Bay | Less than 20,000 SF

Small Bay facilities are multi-tenant buildings often leased by local trades or small e-commerce operators. Think of the everyday HVAC contractor in Wisconsin or a local bakery distributor in Dallas. The tenant base is filled with “mom-and-pop” operators with weaker credit but strong local roots. It’s more than likely you know a family friend who rents space in a Small Bay property.

- Specifications: Shorter bay depths, lower clear heights (14-20 ft), limited dock doors, higher office-to-warehouse ratios.

- Lease Terms & Structures: 1–3 year terms with gross or modified gross structures where landlords cover structural items and many operational expenses (OpEx) due to tenant size.

- Tenant Base: Plumbers, HVAC, electricians, small distributors, local e-commerce startups.

- Investor’s Lens

- Positives: Premium rent per square foot (often 20%+ above Bulk), resilient tenant demand with national vacancy below 5% due to limited new development, strong diversification across many small tenants.

- Risks: High turnover, weaker credit tenants, shorter Weighted Average Lease Terms (WALT), exposure for OpEx and more hands-on management.

Shallow Bay | 20,000–100,000 SF

Shallow Bay quite possibly offers the best value in this list. These properties serve as the “next step” for regional operators who have outgrown small bays but not yet into bulk distribution. The facilities are common in suburban infill markets and appeal to investors due to the scarcity of available inventory and the average time to lease being 5.7 months as compared to 7.8 months in BigBulk industrial.1

- Specifications: 20-28 ft clear heights, bay depths 140-200 ft, multiple dock-high doors, and flexible layouts for multi-tenanting.

- Lease Terms & Structures: 3-7 year terms mostly structured as Triple Net (NNN) or Modified Gross – tenants cover taxes, insurance, and utilities, landlords cover structural items.

- Tenant Base: Regional distributors, light manufacturers, and scaling e-commerce brands.

- Investor’s Lens

- Positives: Better risk-adjusted returns and stability with cap rates between 6.0-6.5%, higher rents per square foot, and greater diversification across many tenants.

- Risks: Tenant build-outs can be costly, and rollover can still occur more frequently than with larger tenants and longer leases.

Lightstone Case Study: Lightstone acquired a shallow bay property in Central Pennsylvania in the first quarter of 2025, which consists of three buildings over 142,900 square feet. This property has strong multi-tenancy with five tenants and is succeeding even with in place rent at a 25% discount to the market. It was an opportune buy as we are already a prominent owner in the area.

Last Mile | 10,000–50,000 SF

Last-mile warehouses are the small, in-town facilities that keep e-commerce moving.They’re the buildings that get packages from a regional hub to your front door. Most sit inside or just outside major metro areas. Specs are often dated — lower ceilings, limited docks — and land costs are high. But being close to the consumer outweighs those flaws. Tenants will pay a premium for proximity, and there’s virtually no way to build more of these in dense markets.

- Specifications: 10,000–50,000 SF, older buildings with 14–20 ft clear heights, limited docks, sometimes just grade-level loading.

- Lease Terms & Structures: 3–5 years, usually modified gross or NNN; older buildings often leave landlords covering more OpEx.

- Tenant Base: Parcel carriers, grocery distributors, e-commerce delivery operators.

- Investor's Lens

- Positives: Premium rents, tenants rarely leave once established, strong and steady demand tied to e-commerce.

- Risks: Expensive to buy, no room to scale, constant CapEx needs, limited tenant pool.

Lightstone Case Study: Lightstone owns a last-mile building in Brooklyn. It has just 18-foot ceilings and minimal dock space, but it stays full because it’s minutes from Manhattan. One parcel carrier and a regional grocer lease the space, both unwilling to risk losing such a prime location.

Bulk Distribution | 100,000–500,000 SF

Bulk Distribution centers are the backbone of regional supply chains — the large-format warehouses you’ll often see along interstates or near airports.These facilities are designed for throughput and efficiency, serving retailers and 3PLs moving goods across metro areas or regions.

- Specifications: 28–36 ft clear heights, deep bays (180–250 ft), wide truck courts, high dock ratios, trailer parking.

- Lease Terms & Structures: 5–10 year NNN leases, tenants cover most OpEx. Predictable and lower-risk income streams.

- Tenant Base: Third-party logistics (3PLs), regional distributors, national retailers.

- Investor’s Lens

- Positives: Strong credit tenants, predictable cash flow, assets positioned along key logistics corridors.

- Risks: Tenant concentration (a single vacancy can create large income gaps), longer downtime if vacant, lower PSF rents vs. shallow bay.

Lightstone Case Study: Lightstone’s Charlotte and Raleigh-Durham portfolio (652,000 SF across five buildings) was an excellent bulk investment. With bay depths over 200 feet and 30 ft clear heights, these properties are ideal for logistics users. At the time of acquisition, rents were 27% below market — creating immediate upside through lease-up and rent resets.

Big Box | More than 500,000 SF

Big Box assets are the “flagship” warehouses — 500,000 SF+ facilities built for Fortune 500 companies. These are highly visible, often custom-designed distribution centers for national supply chain operators.

- Specifications: 500,000–1M+ SF, 36–40 ft clear heights, dozens of dock doors, heavy power supply, massive trailer storage.

- Lease Terms & Structures: 10–20 year NNN leases, tenants typically carry all OpEx.

- Tenant Base: Fortune 500 retailers, e-commerce giants, institutional-grade users.

- Investor’s Lens

- Positives: Long leases, credit tenants, highly liquid in institutional markets, stable cash flows.

- Risks: High tenant concentration (loss of anchor tenant = major income disruption), limited replacement pool, high capital entry point.

Lightstone Case Study: Lightstone’s Texas Big Box distribution center, over 600,000 SF, is leased long-term to a national and publicly traded furniture, appliance, and electrics retailer with more than 160 stores around the country. Despite requiring significant upfront capital, the property provides stable income with minimal landlord responsibilities thanks to its long NNN lease.

Specialized / Cold Storage / Manufacturing

Specialized assets are “mission-critical” properties — cold storage for food and pharma, or advanced manufacturing plants requiring heavy power. These are hard to replicate, sticky by design, and command premium rents because tenants invest heavily in customization.

- Specifications: Cold storage is refrigeration and insulation, while manufacturing is heavy power, cranes, and reinforced floors, which are often costly to retrofit.

- Lease Terms & Structures: 10+ year NNN leases; tenants absorb most OpEx due to high customization.

- Tenant Base: Food logistics operators, pharmaceutical distributors, advanced manufacturers.

- Investor’s Lens

- Positives: High tenant stickiness, long leases, premium rents, and critical to supply chains.

- Risks: Expensive to reconfigure, small replacement tenant pool, functional obsolescence risk if tenant vacates.

Investment Profile Takeaway

Each industrial subtype plays a unique role to an investor. Small Bay and Specialized assets deliver higher yields but come with more rollover and re-leasing risk. Shallow Bay and Bulk provide balance — steady income with enough turnover to capture rent growth. Last Mile and Big Box serve as anchors, offering stability from credit tenants and locations that are hard to replace.

It’s worth noting that while investors could assume multi-tenant Shallow Bay is safer, the cash flow dynamics can tell a different story. Shallow Bay assets frequently trade in the 6.0–7.0% cap rate range, while larger single-tenant buildings can trade north of 7.0% because of perceived concentration risk. In reality, those large assets often produce more stable cash flow thanks to longer leases and stronger tenant credit.

In today’s market, focus matters. Infill Small and Shallow Bay assets are scarce, which drives rent growth. Bulk and Big Box continue to attract credit tenants that want modern specs and longer leases. Specialized assets, like cold storage and advanced manufacturing, are niche opportunities but increasingly important as supply chains shift closer to home.

Lightstone DIRECT brings investors the opportunity to diversify into Industrial, at a time when many self-directed investors are long on multifamily. Given Lightstone’s operational breadth and experience within the sector, Lightstone DIRECT also offers the opportunity to tap into different industrial subtypes, and types of industrial asset that align most with Lightstone’s current thesis.

Conclusion: Lightstone DIRECT’s Offering

At Lightstone DIRECT, we believe the best portfolios blend growth with durability. That means a focus to balance high-yield, shorter-term Shallow Bay investments in infill markets with the stability of Bulk and Last Mile, and the long-term security of Big Box and Specialized facilities.

For individual investors, this creates access to an institutional-quality portfolio: exposure to secular demand drivers like e-commerce and reshoring, while maintaining downside protection through diversification and credit-backed leases. Industrial isn’t just about “warehouses” — it’s about knowing which type, in which market, with which tenant will deliver the right balance of yield and stability. That’s the strategy we’ve built, and the one we’re proud to bring to investors.

[1] JLL: US Shallow Bay Industrial Report – Spring 2025

Storm Murphy

Storm Murphy is Associate Director of Capital Formation at Lightstone DIRECT, where he helps lead the firm’s capital raising efforts across its multifamily and industrial investment platforms. He combines investment strategy, financial acumen, communication, and strategic marketing to enhance the investment experience for high-net-worth individuals, RIAs, and family offices.

Before joining Lightstone, Storm raised capital across the Midwest in the multifamily space. He holds a Bachelor's in Finance from Wofford College, where he captained the Division I basketball team to an NCAA Tournament appearance and later helped lead Virginia Tech to an ACC Championship. He brings the same leadership, discipline, and competitiveness developed on the court to his work in capital markets. Outside of the office, he’s an avid golfer and enjoys playing Texas Hold’em.