Learn more about everything Lightstone DIRECT has to offer

Generating magic link...

Equity Waterfalls in Private Real Estate: How Distributions Work

Equity waterfalls are a standard feature of private real estate syndications. They outline how cash flow and profits are distributed between limited partners (LPs) and the sponsor (GP). While the concept is straightforward, the details matter. The waterfall determines the order in which parties are paid, how return thresholds are applied, and when the sponsor begins participating in the upside through the promote.

For investors, understanding the waterfall is useful for two reasons. First, it clarifies how the deal is structured and how incentives are designed. Second, it helps investors interpret projected returns more accurately, since a sponsor’s target IRR or equity multiple is ultimately distributed through this framework, not outside of it.

Why Waterfalls Exist

Private real estate is typically structured as a partnership. LPs contribute equity, while the sponsor is responsible for sourcing the opportunity, executing the business plan, and managing the investment through the hold period.

The waterfall exists to formalize how the partnership shares cash flow and profits. Most structures are built so that LPs receive priority distributions up to a baseline return, and the sponsor’s share of profits increases only after certain performance thresholds are met. This is one of the primary ways private real estate structures align incentives between investors and operators.

How the Preferred Return Works

Most real estate waterfalls include a preferred return (pref.). The preferred return is generally the hurdle rate that must be satisfied before the sponsor participates materially in profits through the promote.

In practice, the preferred return functions as a distribution priority. It is often structured as an annual percentage, and it may accrue if it is not fully paid in a given period. The specific mechanics vary by deal, including whether the pref is cumulative or compounded, but the underlying purpose is to establish an initial hurdle that prioritizes investor returns before GP incentive compensation begins.

It is also important to view the preferred return correctly. A preferred return is not the same thing as a guaranteed return. It simply defines priority and sequencing. If cash flow is limited early in a hold, the preferred return may accrue, but it still depends on overall performance and available proceeds.

How Tiered Splits Work

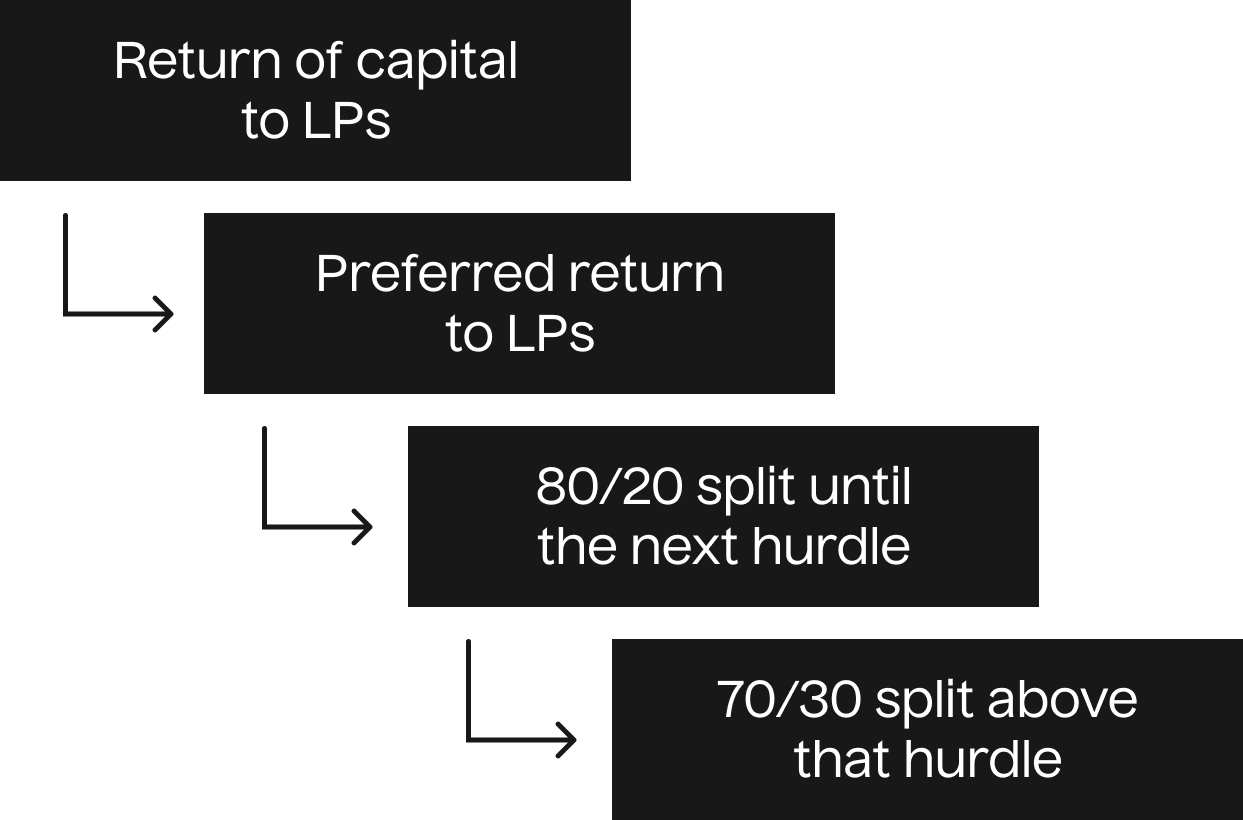

After return of capital and the preferred return, many offerings shift into tiered profit splits. This is what most people mean when they refer to a “waterfall.”

Tiers are built around return thresholds, commonly based on IRR and sometimes equity multiple. As those thresholds are reached, the sponsor’s share of profits, the promote, typically increases.

A simplified example might look like this:

The exact tiers and hurdle levels vary across sponsors and strategies, but the structure generally follows the same logic: early cash flow and baseline returns are prioritized for investors, while outperformance increases sponsor participation.

For investors, it’s important to look beyond the headline split and understand how much capital the sponsor has invested alongside LPs. The same 80/20 promote can be meaningfully more or less dilutive depending on the sponsor’s co-investment.

Catch-Up Clauses and Their Role

Some waterfalls include a catch-up provision. Catch-ups typically come into play after the preferred return is satisfied.

The purpose is to help the sponsor reach the intended promote economics once investors have received their priority return. In a catch-up tier, the sponsor may receive a larger share of distributions for a period of time until the overall profit split reaches a stated ratio, after which the waterfall moves into its longer-term split tiers.

Catch-ups are less about changing the ultimate destination and more about changing the path. Even when the final profit split is similar, the presence of a catch-up can affect timing, particularly in the mid-years of a hold period. For investors, understanding the catch-up tier is useful for interpreting how cash flow may be allocated once the preferred return threshold has been achieved.

How Sponsors Participate in Upside

The promote is the sponsor’s share of profits above certain return thresholds. It is a core part of most private real estate structures because it is intended to reward strong execution and outcomes.

Promotes are typically structured as a percentage of incremental profits and often increase across tiers, which is why deal returns can scale meaningfully for sponsors once higher hurdles are reached.

Because the promote is earned through the waterfall, investors should view it in context with the full distribution sequence. A promote that begins only after capital and a baseline return are delivered generally reflects a more investor-prioritized structure than one that begins earlier or is heavily accelerated through catch-up language.

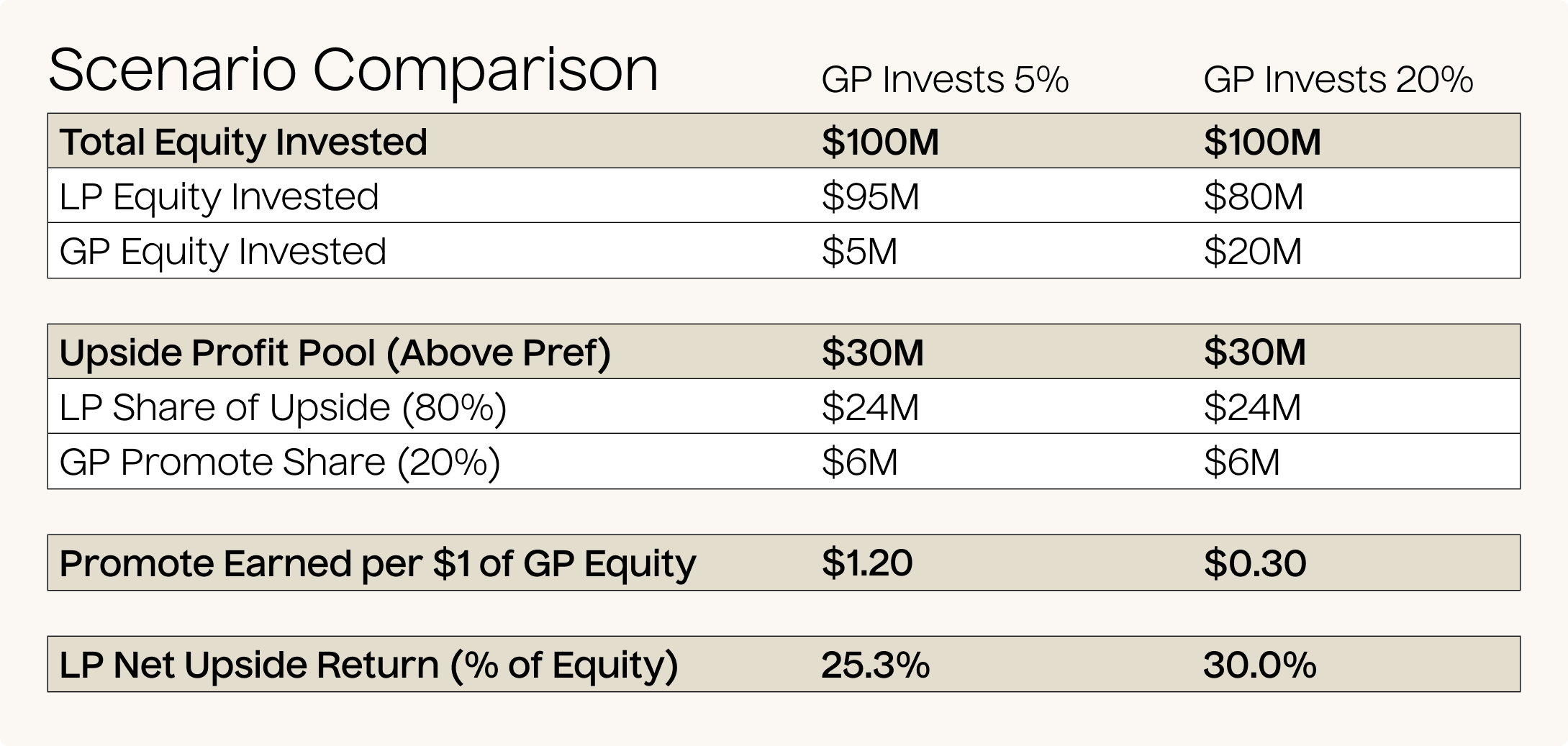

Sponsor co-investment affects how dilutive a promote is to investors, even when the headline terms are the same. In an 80/20 structure after an 8% preferred return, LPs may be paying the same 20% promote, but their net upside depends on how much equity they contribute relative to the sponsor.

It also affects how much incentive compensation the sponsor is earning per dollar invested: in this example, a sponsor investing 5% earns $1.20 of promote for every $1 of equity contributed, compared to only $0.30 per $1 invested when the sponsor contributes 20%.

For LPs, the same 20% promote is more dilutive when the sponsor invests less capital, because the LPs are sharing the same profit pool while contributing a larger portion of the equity—reducing their net upside return (25.3% vs. 30.0% in this simplified example).

It is also helpful to separate promote economics from fees. Fees generally cover the operational responsibilities of sourcing, closing, and managing an investment, and they are typically paid throughout the hold period. The promote, by contrast, is tied directly to performance and becomes meaningful only if the deal clears the thresholds outlined in the waterfall.

Both affect net returns, but they serve different purposes. Fees compensate execution. Promote compensates outperformance. A clean structure makes it easy to see the difference.

Why Clawbacks Matter

Clawbacks are designed to ensure that promote distributions remain consistent with the agreed waterfall economics over the life of the investment.

If a sponsor receives promote distributions during the hold period, for example following strong early performance or a capital event, later outcomes could reduce the overall return below what would have supported that level of promote. A clawback provision is a mechanism that can require the sponsor to return any excess promote so that the final distribution aligns with the intended tier structure.

Not every structure uses clawbacks in the same way, but the underlying objective is the same: it protects the integrity of the waterfall by tying sponsor economics to final performance rather than interim outcomes.

The Bottom Line

A private real estate waterfall is simply the distribution framework that governs who gets paid, in what order, and under what conditions. It is also one of the clearest places to evaluate alignment between LPs and sponsors.

Most waterfalls follow the same core sequence: return of capital, preferred return, and then tiered promote splits that increase sponsor participation as performance improves. Features like catch-ups and clawbacks can meaningfully affect timing and investor protection, which is why they are worth understanding before investing.

While the legal language can be dense, the underlying structure is usually built from a consistent set of principles. The specific mechanics of the preferred return, promote tiers, catch-up provisions, and clawbacks are detailed in the Private Placement Memorandum (PPM) and the operating or LLC agreement for each deal. Once investors understand those principles, the waterfall becomes easier to interpret and compare across offerings.

Annina Vaisanen

Annina Vaisanen is part of the Investor Relations team at Lightstone DIRECT, where she focuses on coordinating and enhancing the investor experience across the platform. In addition to overseeing investor relationships, she also plays a key role in streamlining systems and processes that support efficient operations across the group.