Learn more about everything Lightstone DIRECT has to offer

Generating magic link...

Conservative vs. Aggressive Underwriting: How a 12% IRR Becomes a 17% IRR

Take a look at any projected IRR in any marketing materials of any real estate manager. The font is big and bold. The disclosures of risk factors are usually scant, if there at all. There is little acknowledgement of the highly sensitive nature of IRR projections.

More and more, prevailing IRR projections among real estate managers appear to be exercises in selective optimism, if not magical thinking.

Individual LP investors should keep in mind, always, that IRR projections are, well, projections, synthesizing various inputs and assumptions into a prediction of how the future will look for a given asset and a given market. All models are wrong; some are useful. No real estate manager can predict the future, but the rigor and reasonableness of the manager’s projections may vary quite a bit.

That is why individual LP investors should remain circumspect when looking at projected IRRs, especially when they appear unusually high for a relatively plain-vanilla multifamily business plan. In many cases, it does not take a dramatically better deal, or a dramatically better operator, to move a projected return higher. It takes only a handful of favorable assumptions layered on top of one another: somewhat stronger rent growth, a slightly tighter exit cap, a quicker lease-up, a better-timed sale, or cheaper debt. Each assumption may appear defensible on its own. Collectively, they can transform a conservative 12% projected IRR into a 16% or 17% one.

That is the practical difference between conservative underwriting and aggressive underwriting.

Conservative underwriting does not mean pessimistic underwriting. It means building a model that allows for friction, delay, execution risk, expense pressure, and imperfect market conditions. In other words, soberly assessing all components of the business plan and taking hope out of the equation. Aggressive underwriting, by contrast, tends to treat favorable conditions as the base case. It often assumes that the renovation program stays on schedule, rent premiums arrive on cue, expenses remain contained, debt service stays manageable, and exit pricing cooperates at precisely the right time.

For individual LP investors, a critical eye is absolutely imperative.

The Core of the Matter: IRR is Highly Sensitive

Internal rate of return is a useful metric, but it is unusually sensitive to timing and terminal value. That sensitivity makes it easy to influence. If cash flows arrive earlier, if NOI ramps more quickly, or if the sale price is boosted by a lower assumed exit cap rate, IRR can rise meaningfully even when the business plan itself has not become materially safer. Conversely, permitting delays, a hiccup in leasing strategy, or less favorable capital markets at the point of refinance can all significantly harm ex poste IRR.

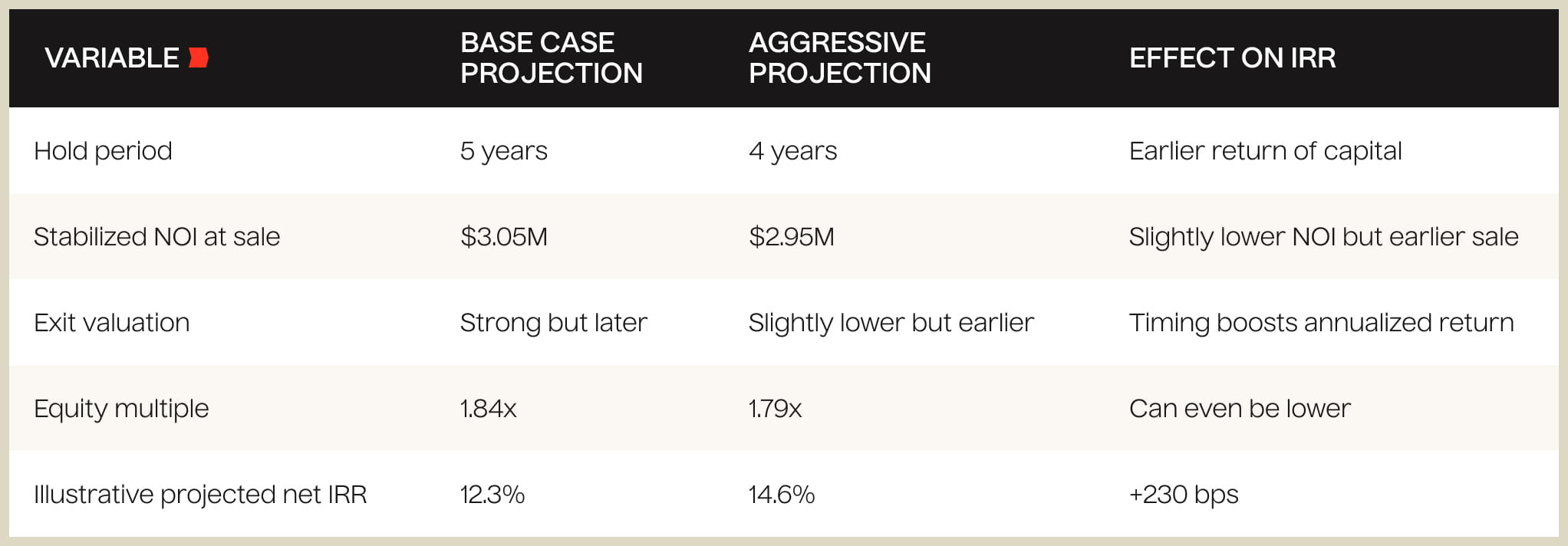

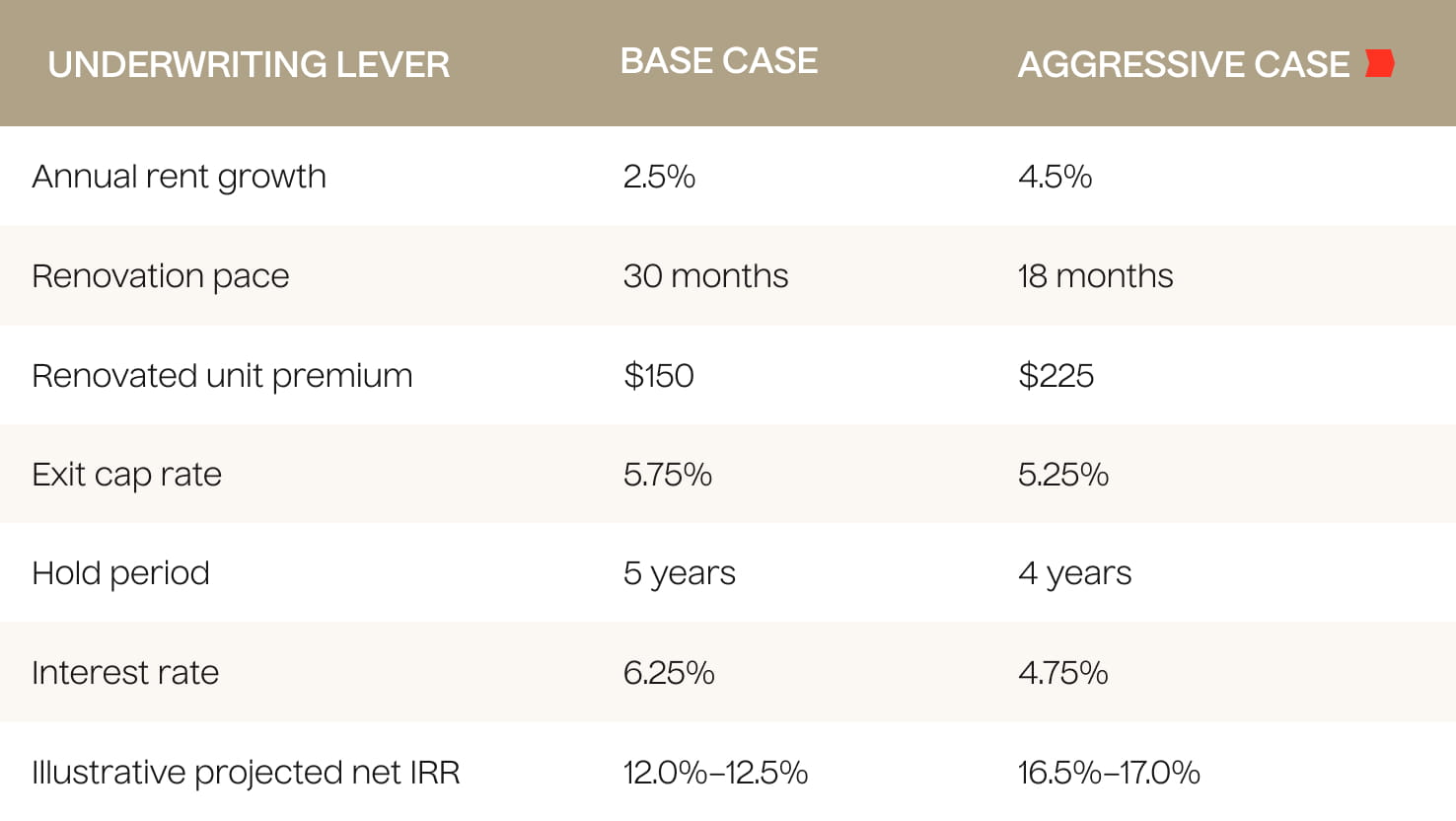

The following scenarios are hypothetical, but they reflect the basic ways IRR is often stretched. In each case, the “conservative” and “aggressive” projections assume the same acquisition, the same asset type, and broadly the same business plan. What changes are the assumptions.

Checklist — What LP Investors Should Really Ask

When presented with a high projected IRR, the right response is not immediate skepticism, but a spirit of inquiry.

- What assumptions are carrying the return?

- How much of the projected upside depends on future market rent growth rather than in-place yield?

- How much depends on the sale (exit) price? Conversely, how much of the total return is accounted for through cashflow, and starting from a reasonable baseline?

- How much depends on completing renovations on time and at budget?

- What happens if exit timing slips by a year?

- What happens if rent growth is average rather than strong?

- What happens if rates stay elevated?

These are reasonable questions that should be clear in offering materials, and/or the manager should be able to speak to. The answers tell you whether you’re looking at disciplined underwriting, or a marketing sleight of hand.

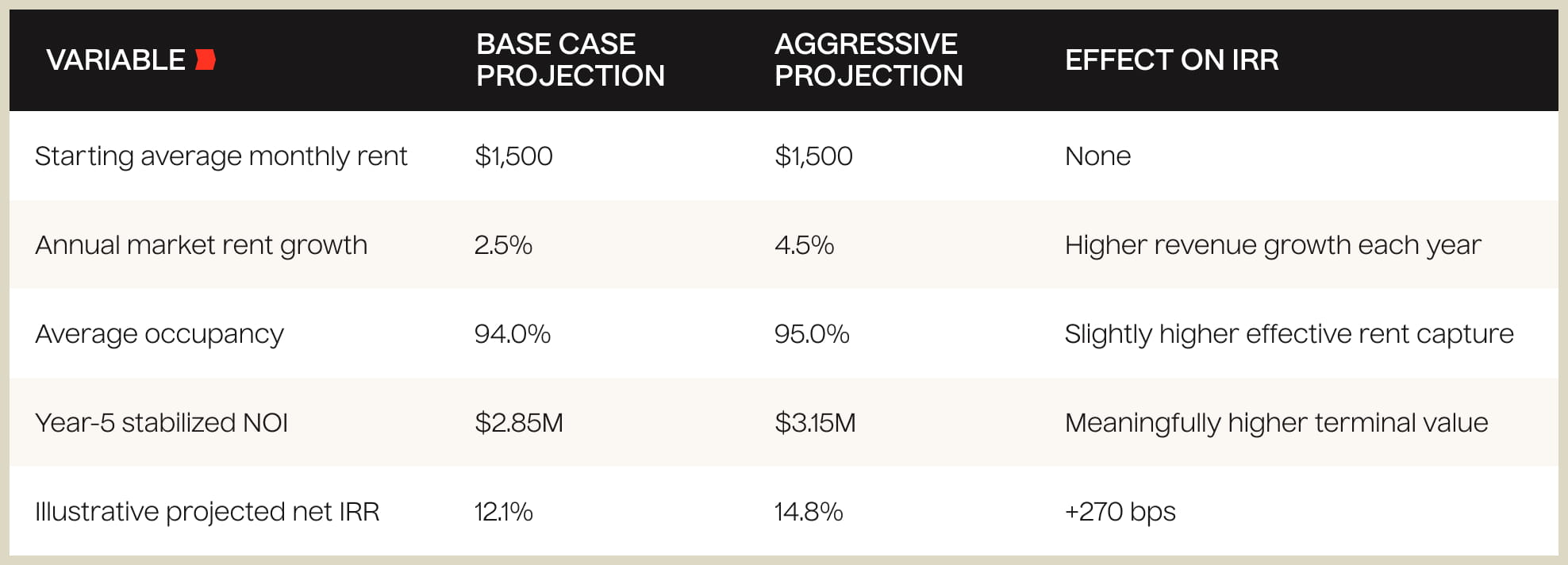

1. Rent Growth: The Easiest Way to Improve a Model

Rent growth is one of the most common ways to enhance projected returns without changing the asset itself.

Suppose a sponsor acquires a 200-unit multifamily property with in-place average effective rent of $1,500 per month. If the model assumes 2.0% to 2.5% annual rent growth, the projected NOI growth may look respectable but restrained. If that assumption moves to 4.0% or 4.5%, however, the impact compounds over the hold period. Because exit value is typically a function of NOI, the more aggressive assumption boosts both interim cash flow and the eventual sale price.

The aggressive version is not necessarily absurd. But it leaves much less room for a softer leasing environment, concessions, local supply pressure, or simple mean reversion in rent growth. Conservative underwriting asks whether the deal still works if revenue growth is merely good rather than exceptional.

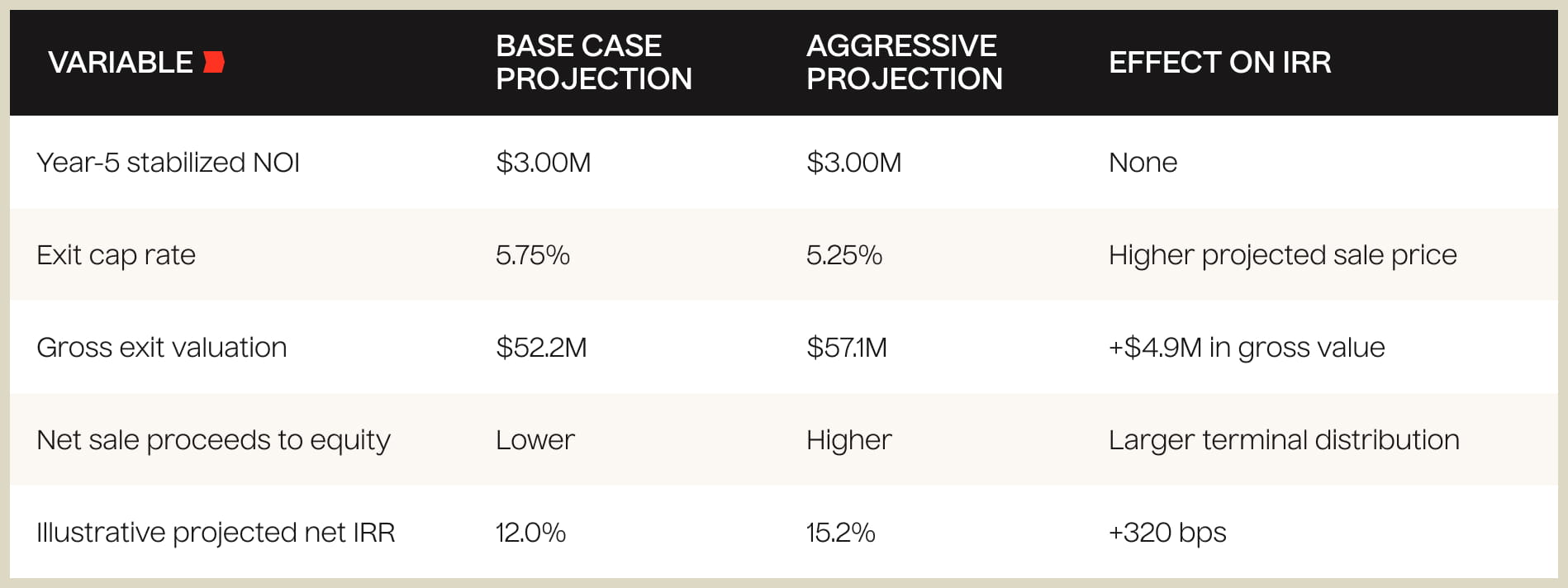

2. Exit Cap Rates: A Small Change with a Large Effect

Nothing can move a model more quickly than the exit cap rate.

A 25- to 50-basis-point change in exit cap assumptions can materially change sale proceeds, particularly if the property’s projected NOI has already been expanded through optimistic operating assumptions. This is why investors should scrutinize not only the exit cap itself, but whether the projected sale price depends on a future buyer paying a premium valuation in a cooperative capital markets environment.

This is often where “storytelling” enters underwriting. A sponsor may justify the tighter exit cap by pointing to future market maturation, expected rate cuts, better asset quality after renovations, or stronger buyer demand. Sometimes that will happen. But it is also the purest example of a return projection leaning on conditions the sponsor cannot fully control. After all, no one can predict the future. Whereas rents and occupancy start with an observed reality, exit cap rate projections are describing a fully hypothetical future. High-quality GPs will model exit cap rates in a data-driven manner, but still approach the matter with a high degree of humility and consider various scenarios in terms of the impact various exit caps would have on total deal return.

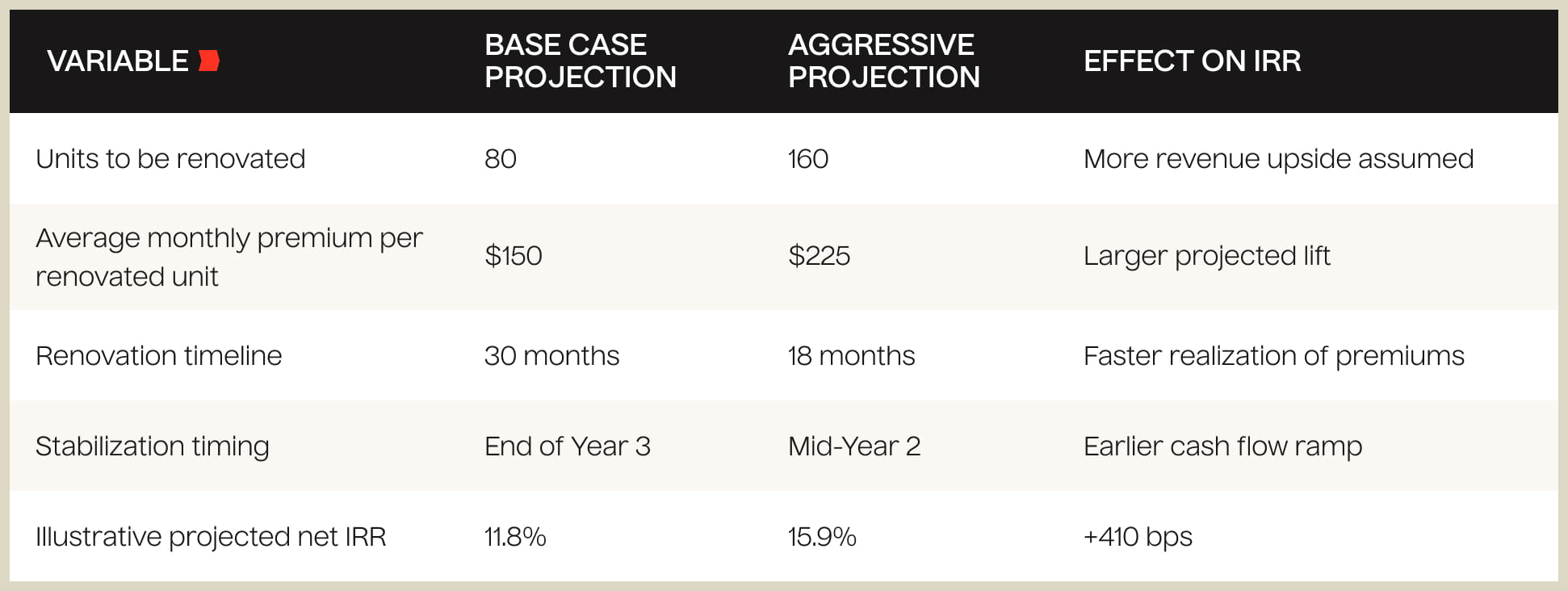

3. Lease-up Timing and Renovation Pace: Timing Does a Lot of Work

IRR gives disproportionate credit to earlier cash flows. That means faster lease-up and quicker renovation execution can have an outsized effect on projected returns.

A value-add deal may look modestly different on paper if unit upgrades happen in 24 months instead of 36. In the real world, that difference can hinge on labor availability, contractor performance, permitting, tenant turnover, and local competition. Yet the model often treats the faster timeline as routine.

This is one of the clearest examples of how “aggressive” does not need to look reckless. A sponsor can simply assume that more units are renovated, at higher premiums, on a faster schedule. None of those inputs may look shocking on its own. Together, they can dramatically lift the projected IRR.

4. Exit Timing: One of the Quietest Ways to Inflate IRR

Sometimes the easiest way to improve IRR is simply to shorten the hold.

Selling in year four instead of year five can increase the annualized return even if the total dollar profit does not improve proportionately. Mathematically, that is valid. But economically, it can be misleading if the model assumes that the property will be sold during an ideal market window rather than whenever market conditions ultimately allow.

This is a useful reminder that IRR is not the same thing as total wealth creation. A deal can show a higher IRR with a similar, or even slightly lower, equity multiple if the capital comes back faster.

5. Interest Rates: Same Leverage, Very Different Outcomes

This issue deserves special attention in the post-2022 environment.

In an era of very cheap debt, many business plans were more forgiving. Sponsors could underwrite thinner spreads, count on lower carry costs, and rely on refinancing flexibility that is much harder to assume today. Even at the same leverage, a materially higher borrowing cost can reduce distributable cash flow, make debt service tighter, and compress projected exit proceeds because future buyers are also underwriting against a higher cost of capital.

This is critical because many aggressive models implicitly assume some version of debt relief: lower future rates, cheaper refinancing, or financing terms that make the carry more manageable than current conditions would suggest. In earlier cycles, those assumptions may have felt less heroic. Today, they deserve closer scrutiny.

This input is especially important if the sponsor is taking on floating rate debt.

How the 12 Becomes the 17

What happens if several of these inputs move from conservative to less-conservative?

A model does not need to rely on one glaringly unrealistic assumption. It can get to an aggressive result by combining several mildly optimistic ones:

That is how a “good” deal becomes a “great” one on paper. Not necessarily through deception, but through assumption stacking.

Conclusion: The Direct Take

Reasonable underwriting is not about suppressing upside. It is about respecting uncertainty.

In multifamily investing, there is nothing inherently suspicious about a projected 17% IRR. But there is also nothing inherently reliable about it. A projected return is only as durable as the assumptions beneath it and the team responsible for executing on the business plan. As a return metric, IRR in particular is highly responsive to optimism around growth, timing, and terminal value.

That is why disciplined investors should focus less on the headline return and more on the architecture of the model. In many cases, the difference between a 12% IRR and a 17% IRR is not a fundamentally different asset. A more conservative number is about soberly modeling in uncertainty; an aggressive number reflects a willingness to assume that almost everything will go to plan.

The best underwriting does not ask, “How high can we make this number?” It asks, “What happens when reality is slower, messier, and less cooperative than the most optimistic version of the model?”

A conservatively underwritten IRR, above all, is about reducing magical thinking. In other words, how does this deal look if none of our optimistic scenarios come to pass? Can we still live with it, and is the IRR figure still compelling on a risk-adjusted basis given alternative opportunities at any given moment in the market. This approach may not make for eye-catching subject lines in marketing emails. And conservative underwriting, with responsible leverage, may not pencil to the type of IRRs that were shopped around pre-2022, prior to rates and input costs rising rapidly.