Best Places to Invest $100K in 2026

Where’s the best place to invest $100K in 2026? There’s no one right answer, and it depends on any given investor’s liquidity, risk tolerance, time horizon, and preexisting portfolio. Let’s start with the assumption that you are making all the conventional moves already – maxing out your 401K, investing in a 529 plan if you have dependents, etc. Perhaps you already have a rental property or two, and have discretionary allocations to individual stocks, cryptocurrency, private credit, or other alts. Or, perhaps you are just beginning to diversify away from something that looks more like a traditional 60/40 portfolio. What is the best way to invest $100K or more in today’s market?

Having $100K to invest is a good place to be, in any market. But 2026 is not a straightforward market landscape for a self-directed investor to operate in. You're operating in one of the more complex market environments in recent memory. The S&P 500 closed 2025 with a respectable 17.9% total return, but that headline number conceals a year of whiplash—tariff shocks, geopolitical flare-ups in the Middle East, and an ongoing tug-of-war between the White House and the Federal Reserve over monetary policy. Equity valuations remain stretched, with the S&P 500's forward earnings yield sitting nearly even with the 10-year Treasury, compressing the equity risk premium to almost zero. Meanwhile, high-yield savings accounts still offer around 4%. The energy shock induced by Middle East conflict caused inflation to flare back up over 3% in March, 2026, potentially portending another bout of persistent inflation, and complicating the Fed’s plans to ease rates several times in 2026.

There’s always the old playbook – dump any excess liquidity into index funds and check back in a few years. If you are a highly risk-averse or time-strapped investor, this is always a reasonable play. However, the smart money today may be able to find pockets of opportunity, and self-directed investors may consider defensive bets in private markets. If you’re looking for a place to park $100K in 2026, look for structural advantages: income, alignment, and downside protection.

Let’s dive in.

Note, this article is for informational purposes only and does not constitute investment advice.

Start with the Boring Stuff: Cash and Fixed Income

Any financial planner will tell you that before you invest aggressively, you should have liquidity in place. With high-yield savings accounts from online banks paying roughly 4% APY with no market risk, there's nothing wrong with parking surplus capital in cash equivalents. It won't build generational wealth, but it gives you optionality and peace of mind while you deploy the rest.

Short-term Treasuries and investment-grade bond funds also deserve a look. The Fed's expected rate cuts could push bond prices up modestly, and you lock in real yields that have been positive for the first time in years. For investors who can stomach slightly more duration risk, intermediate-term bond funds or short-term notes offer a reasonable complement to equities without the stomach-churning swings.

Index Funds Still Belong in the Conversation

Despite elevated valuations, broad-market index funds remain the bedrock of any long-term portfolio. The S&P 500 has compounded at roughly 10% annually over the past century, and that math hasn't changed just because 2026 feels uncertain. Dollar-cost averaging into a low-cost total market ETF—something tracking the S&P 500 or a total U.S. market index—remains one of the most empirically supported strategies available. Fees matter here: a 2% annual expense ratio can erode roughly 30% of cumulative returns over a working career when you factor in compounding. Stick with funds that charge well under 0.10%.

That said, concentration risk is worth flagging. Technology and a handful of mega-cap names have driven the lion's share of recent index returns. Several analysts have noted a rotation toward broader market participation in early 2026—smaller companies, energy, and biotech leading while some of the "Magnificent Seven" have lagged. A tilt toward equal-weight or mid-cap funds could provide better diversification than a capitalization-weighted index alone.

The Case for Private-Market Real Estate

Here is where $100,000 starts to unlock options that smaller portfolios can't access. Private real estate—investing directly in physical properties alongside an experienced operator, rather than buying shares of a publicly traded REIT—has historically offered accredited investors a compelling blend of income, appreciation, and inflation protection. These attributes may be especially relevant in today’s market.

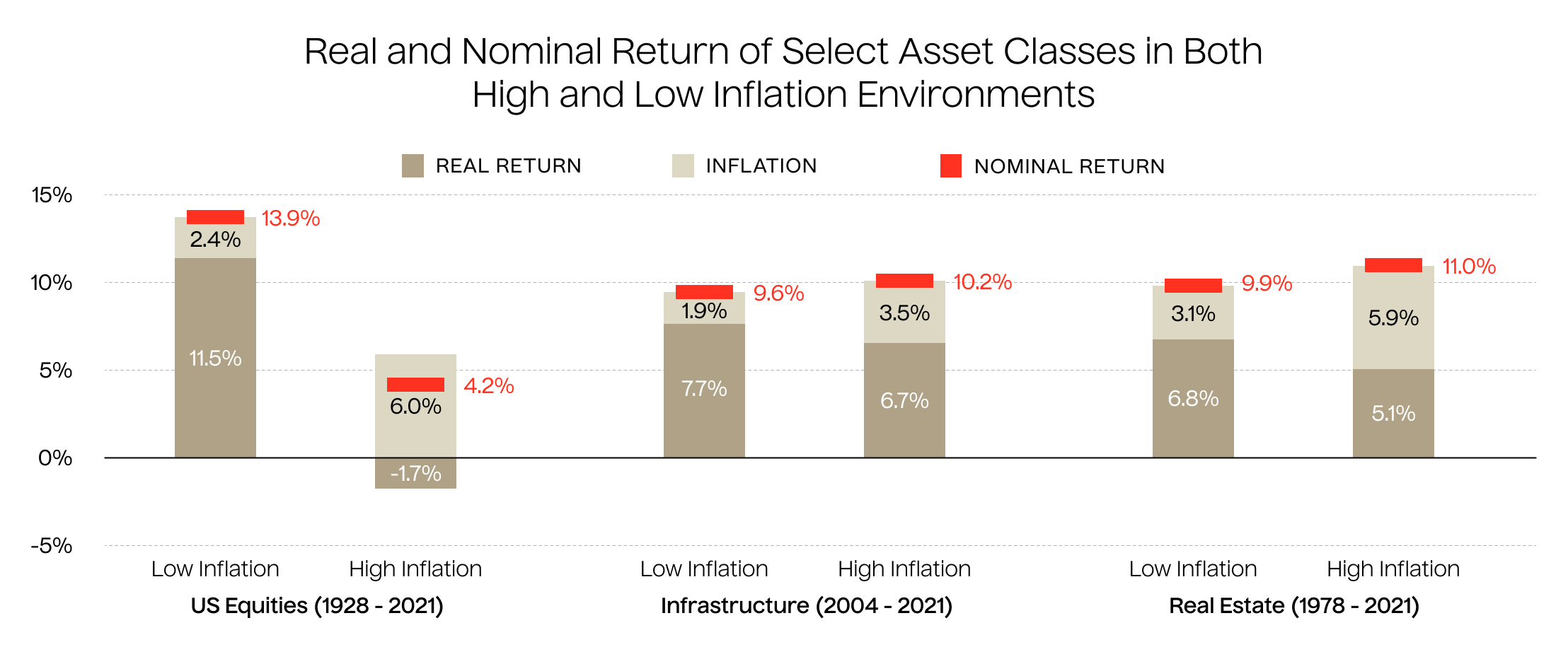

In fact, with global energy markets again in focus, it may be instructive to look back at lessons from the late ‘70s. In fact, across several periods and numerous studies, the data shows that private-market real estate tends to outperform public equities during inflationary periods.

The structural case is straightforward. America is chronically undersupplied on housing. Homeownership is out of reach for a growing share of households, with mortgage rates still elevated and home prices stubbornly high. That means more people renting for longer, and demand for rental housing growing steadily. According to PwC and the Urban Land Institute's 2026 Emerging Trends in Real Estate report, multifamily has the highest-rated investment prospects of any core commercial real estate property type heading into this year, second only to the mixed-use/alternative category, which includes data centers.

On the supply side, the numbers are even more favorable. New multifamily construction has fallen sharply. Only about 270,000 new apartment units are expected to be completed in 2026, the slowest supply growth in over a decade, as permits and construction starts have dropped across every region. That contraction is already supporting stable-to-rising occupancy rates and giving landlords pricing power they haven't had since the pandemic-era boom.

Marcus & Millichap's 2026 National Multifamily Investment Forecast points to renewed momentum: improving capital markets, a sharp pullback in new development, and continued demand for rental units are the three pillars of the positive outlook. CBRE's research confirms this direction, noting that the national vacancy rate of 4.4% remains well below the 2010–2019 average of 5.2%, with operators focused on preserving occupancy through strategic lease renewals.

Meanwhile, roughly $162 billion in multifamily loans are set to mature in 2026—a 56% increase from the prior year. That maturity wall will force some overleveraged owners into refinancing stress or even forced sales, creating acquisition opportunities for well-capitalized buyers who can move with conviction.

Why Operator Alignment Matters

Not all private real estate is created equal, and this is where many less experienced LP investors can make a mistake. The difference between a good deal and a bad one often comes down to one question: is the operator investing their own money alongside yours?

The concept is simple but powerful. When an operator co-invests significant capital into every deal, their financial incentives mirror yours. They're not just collecting management fees—they're risking their own money on the same outcome. This is the kind of structural alignment that separates institutional-quality investment platforms from the crowdfunding sites that proliferated during the low-rate era and have since struggled.

If you have $100K to invest, you may be able to unlock passive investment alongside higher-quality managers.

Lightstone DIRECT is one example of this model in action. When you invest $100K in a single-asset multifamily or industrial a $12 billion-plus AUM owner/operator with a four-decade track record—offers accredited investors access to the same multifamily and industrial deals the firm pursues with its own capital. Lightstone commits a minimum of 20% co-investment in every offering. That's a meaningfully higher skin-in-the-game threshold than what most real estate investment platforms require, and it creates the kind of alignment that institutional limited partners have always demanded from their general partners. The firm has averaged a 27.6% net IRR and a 2.54x equity multiple on investments realized since 2004. Past performance, of course, doesn't guarantee future results, and all real estate investments carry risk—but it's a track record that speaks to disciplined execution across multiple economic cycles.

Platforms like this let individual investors build a portfolio of specific, single-asset deals rather than pooling into a blind fund. You can see the property, review the business plan, and choose the deals that match your own risk tolerance and timeline. Current offerings on Lightstone DIRECT include both multifamily and industrial assets with projected hold periods around four years and minimum investments of $100,000—well within the range of the capital we're discussing here.

A Note on Industrial Real Estate

While multifamily gets most of the attention, industrial logistics properties deserve mention as a complementary allocation. E-commerce isn't going away, supply chains are restructuring, and onshoring trends driven by trade policy shifts are generating sustained demand for warehouse and distribution space. Vacancy rates remain tight in key logistics corridors, and rental growth has outpaced most other commercial property types in recent years. A well-located industrial asset with strong tenant credit can offer stable income with relatively low operational complexity—a nice counterweight to the more management-intensive multifamily sector.

What About REITs?

Publicly traded REITs are a legitimate alternative for investors who want real estate exposure with daily liquidity. They've historically delivered solid long-term returns and offer the diversification benefits of real property. But there's a catch: public REITs trade like stocks. During the 2022–2023 drawdown, many REIT indices fell 25% or more, even as the underlying property fundamentals remained healthy. If you're investing $100K specifically to escape equity-market volatility, buying a REIT ETF may not accomplish that goal. Private real estate, while illiquid, tends to exhibit far less mark-to-market volatility—you trade daily pricing for smoother returns and a longer-term compounding trajectory.

Putting It All Together

How should you invest $100,000 of discretionary capital in 2026? There’s no one-size-fits-all answer for all investors. Anyone who tells you otherwise is selling something. But the research suggests a few principles worth following.

First, maintain liquidity. Keep a meaningful cash reserve in a high-yield savings account for flexibility and emergency needs. If you have just $100K to invest, do not put all your eggs in one basket, especially if it is an illiquid investment. Second, stay invested in equities for long-term growth, but be thoughtful about concentration risk—consider broadening beyond mega-cap tech.

Third, take advantage of your access to private markets. For accredited investors, this is one of the best setups in a decade for private multifamily real estate: new supply is drying up, rental demand is durable, debt markets are thawing, and disciplined operators are finding value. The key is to invest alongside an operator who has real skin in the game—not just a fee stream.

As a general guidepost, you may want to consider the 20% allocation to illiquid alternatives that many endowments, pensions, and other institutional investors pursue over a long time horizon. This diversification, the thinking goes, helps to insulate against massive public market swings and reduce cross-asset allocation within a portfolio.

The $100K threshold opens doors that weren't available ten years ago, such as allocating to a single-asset multifamily or industrial investment via Lightstone DIRECT, with Lightstone, the GP, co-investing at least 20% of the equity alongside you. In a market that's pricing public equities for perfection and offering almost no risk premium above Treasuries, the case for diversifying into real, tangible assets backed by aligned operators has rarely been stronger. If you have a larger amount of liquidity, $500K, say, then additional diversification within alts may be worth considering, such as diversifying across multifamily and industrial real estate, or different strategies and geographic markets within real estate.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investments carry risk, including the potential loss of principal. Consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.